FINRA Requests Comment on a Proposal to Shorten the Trade Reporting Timeframe for Transactions in Certain TRACE-Eligible Securities From 15 Minutes to One Minute

Summary

FINRA is soliciting comment on a proposal to amend Rule 6730 to reduce the Trade Reporting and Compliance Engine (TRACE) trade reporting timeframe for transactions in all TRACE-Eligible Securities that currently are subject to a 15-minute reporting timeframe. Specifically, members would be required to submit a report to TRACE as soon as practicable (as is currently the case), but no later than one minute from the time of execution, for transactions in corporate bonds, agency debt securities, asset-backed securities and agency pass-through mortgage-backed securities traded to-be-announced for good delivery. As is the case today, FINRA would make information on the reported transactions publicly available immediately upon receipt of the trade report.

Questions regarding this Notice should be directed to:

- Chris Stone, Vice President, Transparency Services, at (202) 728-8457 or email;

- Joseph Schwetz, Senior Director, Market Regulation, at (240) 386-6170 or email; or

- Adam Kezsbom, Associate General Counsel, Office of General Counsel, at (202) 728-8364 or email.

Questions regarding the Economic Impact Assessment in this Notice should be directed to Yue Tang, Senior Economist, Office of the Chief Economist, at (202) 728-8237 or email.

Action Requested

FINRA encourages all interested parties to comment on this proposal. Comments must be received by October 3, 2022.

Comments must be submitted through one of the following methods:

- Online using FINRA’s comment form for this Notice;

- Emailing comments to [email protected]; or

- Mailing comments in hard copy to:

Jennifer Piorko Mitchell

Office of the Corporate Secretary

FINRA

1735 K Street, NW

Washington, DC 20006-1506

To help FINRA process and review comments more efficiently, persons should use only one method to comment on the proposal.

Important Notes: Comments received in response to Regulatory Notices will be made available to the public on the FINRA website. In general, comments will be posted as they are received.1

Before becoming effective, the proposed rule change must be filed with the SEC pursuant to Section 19(b) of the Securities Exchange Act of 1934 (SEA or Exchange Act).2

Background and Discussion

FINRA has collected and disseminated transaction information in fixed income securities through TRACE since 2002.3 Since the implementation of TRACE, the fixed income markets have changed dramatically, including a significant increase in the use of electronic trading platforms or other electronic communication protocols to facilitate the execution of transactions. With these changes, FINRA has been considering ways to provide more timely, granular and informative data to, among other things, enhance the value of disseminated transaction data. For example, earlier this year, the SEC approved a FINRA proposal to append a modifier to a corporate bond trade that is part of a larger portfolio trade when reporting to TRACE.4 FINRA is actively considering a number of enhancements to the TRACE reporting and dissemination framework and whether the evolution of trading platforms, market conventions, or other considerations and developments warrant changes to the data FINRA collects and disseminates through TRACE.5

FINRA rules specify the applicable outer limit reporting timeframe for different types of TRACE-Eligible Securities,6 and these timeframes have been augmented over time in line with changes in the markets. The 15-minute reporting timeframe that is applicable to corporate and agency debt securities7 has been in place since 2005.8 A 15-minute outer limit reporting timeframe currently applies to most transactions9 in corporate bonds, agency debt securities, asset-backed securities (ABS)10 and agency pass-through mortgage-backed securities (MBS) traded to-be-announced (TBA) for good delivery (GD).11

Thus, today, transactions in these securities are generally required to be reported as soon as practicable but no later than 15 minutes from the time of execution and FINRA publicly disseminates information on the transaction immediately upon receipt.12 As discussed in more detail below, FINRA has found that 81.9 percent of trades in the TRACE-Eligible Securities that are currently subject to the 15-minute outer limit reporting timeframe were reported within one minute of execution. In light of the technological advances in the intervening 18 years since FINRA first adopted the 15-minute reporting requirement, including the increase in electronic trading, and the potential transparency benefits of more timely trade reporting, FINRA is seeking comment on whether it is appropriate at this time to reduce the trade reporting timeframe for these securities to one minute. As is the case today, FINRA would make information on the transaction publicly available immediately upon receipt of the trade report.

Proposed Amendments

Rule 6730(a)(1) sets forth the requirements for when trades executed during different time periods throughout the day must be reported to TRACE. Currently, corporate, agency, ABS, and MBS TBA GD transactions executed on a business day at or after 12:00:00 a.m. Eastern Time (ET) through 7:59:59 a.m. ET must be reported the same day, no later than 15 minutes after the TRACE system opens. Transactions executed on a business day at or after 8:00:00 a.m. ET through 6:29:59 p.m. ET must be reported as soon as practicable, but no later than 15 minutes of the time of execution, except for transactions executed on a business day less than 15 minutes before 6:30 p.m. ET, which must be reported no later than 15 minutes after the TRACE system opens the next day (and, if reported on T+1, designated “as/of” with the date of execution). Finally, transactions executed on a business day at or after 6:30:00 p.m. ET through 11:59:59 p.m. ET, or for trades executed on a Saturday, a Sunday, a federal or religious holiday, or other day on which the TRACE system is not open at any time during that day, must be reported on the next business day, no later than 15 minutes after the TRACE system opens (and must be designated “as/of” and include the date of execution).

Consistent with longstanding FINRA and SEC goals of increased transparency and improving access to timely transaction data, FINRA is proposing to amend Rule 6730 to reduce the reporting timeframe for corporate, agency, ABS and MBS TBA GD transactions from an outer limit of 15 minutes to one minute. Specifically, FINRA is proposing to amend Rule 6730(a)(1) to provide that:

- for transactions executed on a business day at or after 12:00:00 a.m. ET through 7:59:59 a.m. ET, firms would be required to report the trade the same day, no later than one minute after the TRACE system opens;

- for transactions executed on a business day at or after 8:00:00 a.m. ET through 6:29:59 p.m. ET, firms would be required to report the trade as soon as practicable, but no later than one minute of the time of execution, except that, for transactions executed on a business day less than one minute before 6:30 p.m. ET, firms would be required to report the trade no later than one minute after the TRACE system opens on T+1 (and, if reported on T+1, designated “as/of” with the date of execution); and

- for transactions executed on a business day at or after 6:30:00 p.m. ET through 11:59:59 p.m. ET, or for trades executed on a Saturday, a Sunday, a federal or religious holiday, or other day on which the TRACE system is not open at any time during that day, firms would be required to report the trade on T+1 no later than one minute after the TRACE system opens (and must designate the trade “as/of” and include the date of execution).

FINRA believes that reducing the reporting timeframe for corporate, agency, ABS and MBS TBA GD transactions may improve transparency and allow investors and other market participants to obtain and evaluate pricing information more quickly—creating a qualitative increase in market transparency for these securities. Facilitating more timely information is one way to improve the value of disseminated transaction data. FINRA is actively considering further enhancements to the TRACE reporting framework and whether the evolution of market conventions or other considerations or developments warrant changes to the data that is collected and disseminated through TRACE.

Economic Impact Assessment

Preliminary Economic Impact Analysis

FINRA has undertaken an economic impact assessment, as set forth below, to further analyze the potential economic impacts, including anticipated costs, benefits, and distributional and competitive effects, relative to the current baseline.

Economic Baseline

FINRA analyzed how long it took dealers and alternative trading systems (ATSs) to report trades under the current 15-minute reporting timeframe using TRACE data from January 2021 to December 2021.13 The analysis measured the time between trade execution time and report time (and in cases where reports were later corrected, to the time of final correction). Most of the analysis focused on transactions executed at or after 8:00 a.m. ET and before 6:15 p.m. ET (when trades must be reported as soon as practicable on that day, but no later than within 15 minutes of the time of execution).

Overall, FINRA found that 81.9 percent of trades across TRACE-Eligible Securities that are currently subject to the 15-minute outer limit reporting timeframe were reported within one minute of execution. When FINRA examined reporting times for these securities by individual reporters, 16.4 percent of reporters submitted 95 percent of their trades within one minute.14 For transactions in corporate bonds, which represented 87 percent of all trade reports in the sample, FINRA found that 82.2 percent of trades were reported within one minute and 18.8 percent of reporters submitted 95 percent of their trades within one minute.

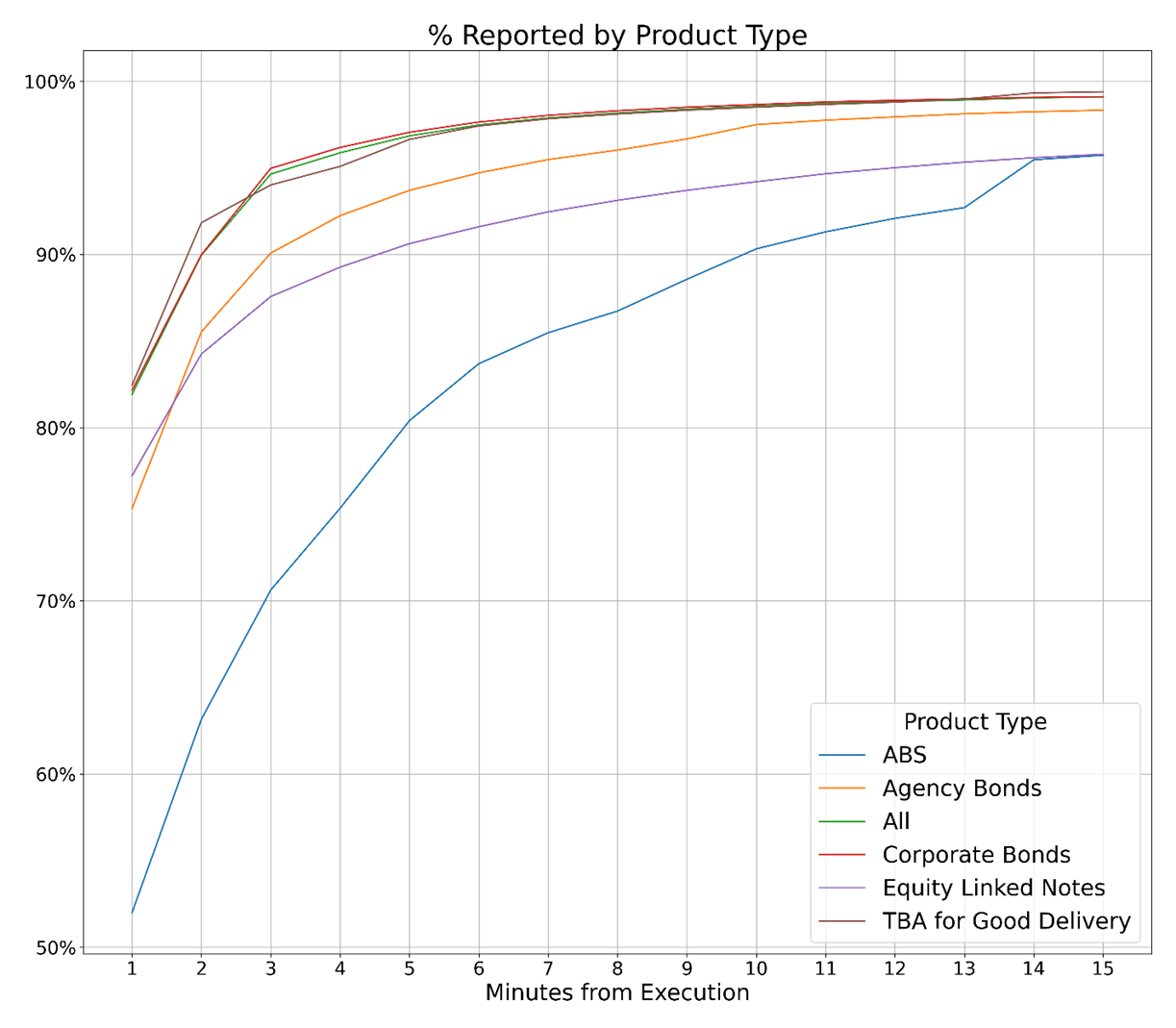

Figure 1 presents the distribution of trade reports from one to up to 15 minutes (in one-minute increments) from the time of execution for ABS, agencies, corporate bonds, equity-linked notes (ELNs) and TBA GD. Figure 1 shows that corporate bonds and TBA GD were reported the fastest among the products, with 82 percent of the trades reported within one minute. ELNs followed close behind at 77 percent and agency bonds at 75 percent. ABS were reported the slowest, with 52 percent reported within one minute.

Figure 1: Reporting Times Across Product Types 15

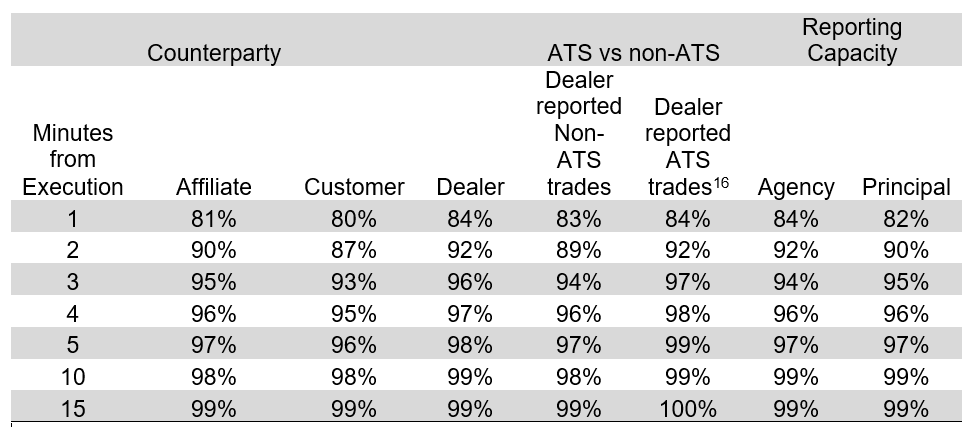

FINRA also specifically examined the reporting timeframe for corporate bond transactions in more depth across bond and reporter characteristics. As mentioned previously, corporate bond trades represented 87 percent of all trade reports in the sample. Table 1 shows that 84 percent of inter-dealer trades were reported within one minute and 80 percent of customer trades were reported within one minute. Dealers reported 84 percent of ATS trades within a minute (dealers reported at a faster pace compared to ATSs, which reported 56 percent within the first minute and 93 percent within the second minute). Eighty-four percent of trades in an agency capacity were reported within one minute, compared to 82 percent of trades in a principal capacity.

Table 1: Reporting Times by Counterparty Types, Platforms, and Reporting Capacity (Corporates)

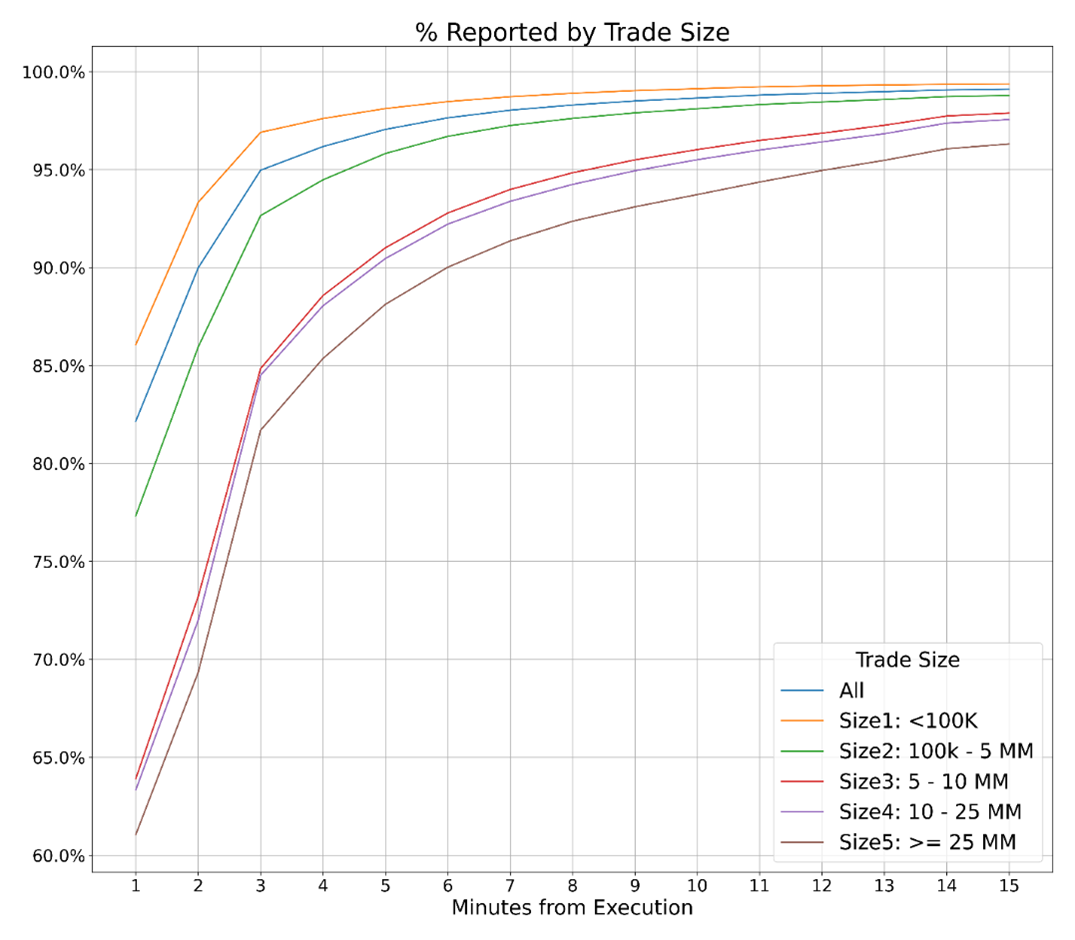

For corporate bonds, FINRA also examined security and trade characteristics that are associated with bond liquidity and how easily bonds can be traded. Figure 2 shows that reporting times differ based on trade size for corporate bond trades. Small trades (trades of less than $100k par value) were, on average reported faster, while larger trades took longer to report. FINRA found that 86 percent of trades smaller than $100k par value and 61 percent of trades larger than $25M par value were reported within one minute. Ninety-eight percent of trades smaller than $100k par value and 88 percent of trades larger than $25M par value were reported within five minutes.

Figure 2: Reporting Times by Trade Size (Corporates)

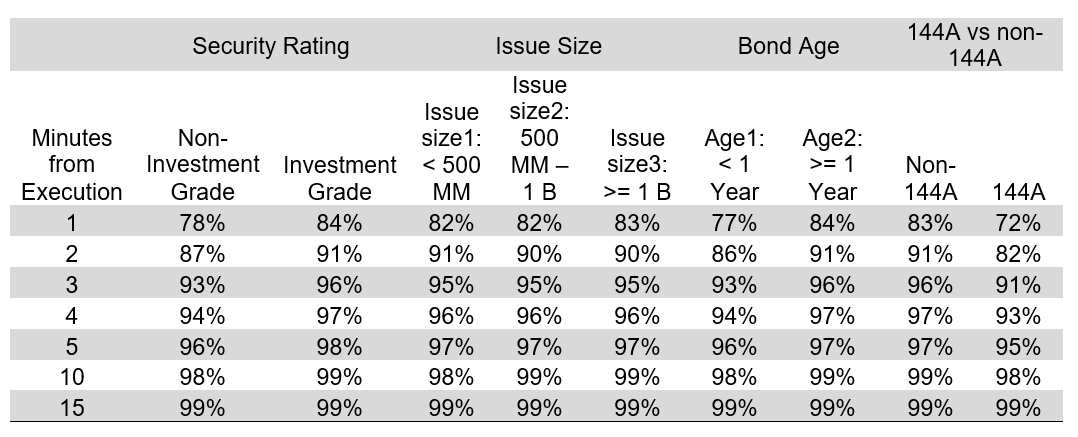

Table 2 shows that trades in investment grade corporate bonds are, on average, reported faster than trades in non-investment grade corporate bonds,17 with 84 percent of trades in investment grade corporate bonds reported within one minute of execution compared to 78 percent of trades in non-investment grade corporate bonds. Younger corporate bonds are usually traded more frequently and are associated with higher liquidity. Table 2 shows that 77 percent of trades in corporate bonds issued less than one year ago were reported within one minute, compared to 84 percent of trades in corporate bonds that were issued one or more years ago. No material differences in trade reporting times existed for corporate bonds of different issue sizes (large issue sizes tend to be more liquid). Seventy-two percent of trades in 144A bonds were reported within one minute, compared to 83 percent of trades in non-144A bonds.18

Table 2: Reporting Times by Bond Grade, Issue Size, and Bond Age (Corporates)

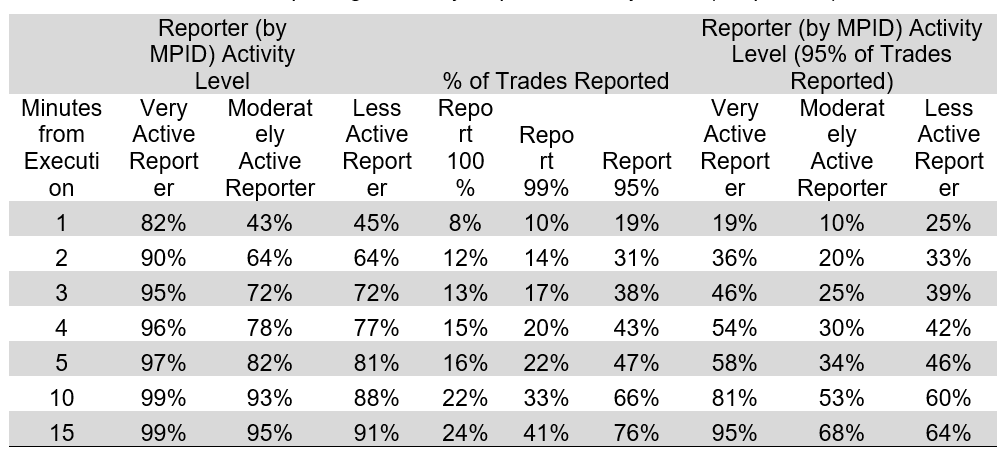

FINRA compared trade reporting times across firms with different levels of activity in corporate bonds in assessing how the potential burdens stemming from the proposal would be distributed across firms. Table 3 shows that, on average, reporters that were more active in trading corporate bonds reported trades more quickly. Specifically, 82 percent of trades executed by more active reporters (with more than 1,000 trades in 2021) were reported within one minute, compared to 45 percent of trades executed by less-active reporters (less than 100 trades in 2021), and 43 percent by moderately active reporters (100 to 1,000 trades in 2021).

FINRA examined the reporting times by individual reporters for corporate bonds in addition to studying the relationship between reporter activity level and report timeframes. Specifically, the analysis measured the cumulative percentage of firms that reported at least a minimum percentage (100, 99 and 95 percentage) of trades at each minute after execution. Table 3 shows that 19 percent of reporters submitted 95 percent of their trades within one minute, 47 percent of reporters submitted 95 percent of their trades within five minutes and 76 percent of reporters submitted 95 percent of their trades within 15 minutes. When examined by reporter activity level, 19 percent of more active reporters submitted 95 percent of their trades within one minute, compared to 10 percent of moderately active reporters, and 25 percent of less-active reporters.

Table 3: Reporting Times by Reporter Activity Level (Corporates)

Very active reporters: more than 1000 trades in 2021; less-active reporters: less than 100 trades in 2021; moderately active reporters: 100 to 1,000 trades in 2021.

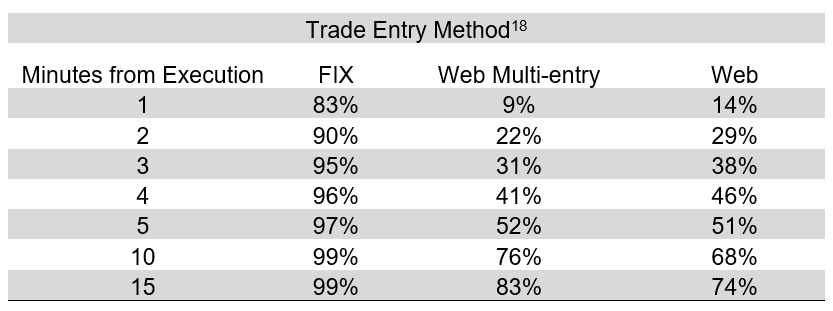

The timeliness of trade reporting is associated with the manner in which the parties enter trade reports to TRACE. Table 4 shows that only 14 percent of the web-entered reports (0.49 percent of all reported trades) were reported within one minute of execution, compared to 83 percent of trades reported via FIX. The analysis did not find that web entry was associated with particular types of trades or the activity level of the reporter. Four percent of more active reporters (357 reporters with more than 1,000 reported trades in 2021) used only the web entry method, 6 percent of moderately active reporters (266 reporters with 100 to 1,000 reported trades in 2021) used only the web entry method, and 10 percent of less-active reporters (345 reporters with less than 100 reported trades in 2021) used only the web entry method.

Table 4: Reporting Times by Entry Method

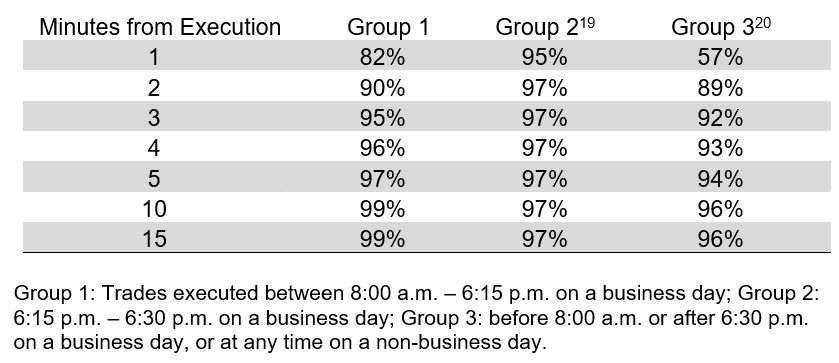

FINRA examined trades in corporate bonds that were executed during TRACE system hours at or after 8:00 a.m. and before 6:15 p.m. ET and compared the findings to trades that were executed outside of these hours. Trades that were executed before 8:00 a.m., after 6:30 p.m., or on a non-TRACE business day represented 1.52 percent of the total trades in corporate bonds reported during the sample period. Of these trades, 57 percent were reported within one minute of the TRACE system open. Trades executed from 6:15 p.m. through 6:30 p.m. on a business day represented 0.02 percent of total trades. Of these trades, 95 percent were reported no later than one minute after the TRACE system opened on the next business day. FINRA did not find a volume or trade size increase immediately after 6:15 p.m.

Table 5: Reporting Times by Time of Day (Corporates)

Group 1: Trades executed between 8:00 a.m. – 6:15 p.m. on a business day; Group 2: 6:15 p.m. – 6:30 p.m. on a business day; Group 3: before 8:00 a.m. or after 6:30 p.m. on a business day, or at any time on a non-business day.

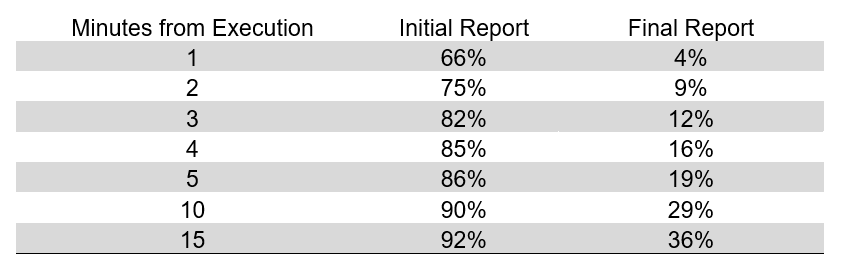

FINRA also examined the reporting timeframes for trade reports in corporate debt securities that were later amended by either a cancellation or a correction because a potential concern with a shorter reporting timeframe is whether it may be associated with a greater error rate or potentially lower quality information. Table 6 presents the reporting times between (i) the time of execution of a transaction and its initial report to TRACE, and (ii) the time of execution and the final report—i.e., the final correction or cancellation. Trade report amendments do not occur often; only 1.2 percent of TRACE trade reports in 2021 were subject to corrections or cancellations after submission. Of these, 66 percent of the initial reports were reported within one minute as compared to 82 percent of the reports that were not subject to a subsequent cancellation or correction, which suggests that faster reporting may not be associated with more errors.22 Trade reports that were later canceled or corrected were initially reported more slowly than reports that were not later cancelled or corrected, possibly reflecting a difficulty in reporting these trades.

Table 6: Reporting Times Adjusted for Cancellations and Corrections (Corporates)

FINRA also assessed trade reporting times for the different types of TRACE-Eligible Securities that are subject to the proposal. Reporting times for agency bonds and corporates were similar, with small trades reported faster and larger trades taking longer to report. When trades in agency debt securities were sorted by trade size, 92 percent of trades in the bottom 20th percentile (by trade size) were reported within one minute, compared to 55 percent of large trades in the top 20th percentile (by trade size). For ABS, most trades (across different sizes) were reported at the same speed; specifically, 44 percent to 48 percent were reported within one minute, except for small trades in the bottom 20th percentile, 77 percent of which were reported within one minute. There was not a significant difference in trade reporting times for TBA trades of different sizes, with 77 percent to 86 percent reported within one minute. In direct contrast to corporate bonds, small-sized ELN trades were reported the slowest.

FINRA found that more active reporters submitted trades more quickly across the different types of TRACE-Eligible Securities subject to the proposal. When reporters were divided into three groups by their total number of trades, very active reporters submitted trade reports the fastest. For example, 30 percent, 41 percent and 52 percent of trades by less-active, moderately active and very active reporters in ABS were reported within one minute, respectively. For agency bonds, the percentages were 45 percent, 45 percent and 76 percent. TBA GD did not show a consistent relationship between the activity level of the reporter and the reporting timeframe, with 64 percent, 54 percent and 84 percent of the less-active, moderately active and very active reporters’ trades reported within one minute, respectively.

When examining reporting timeframes by individual reporters, there was no clear pattern between reporter activity level and reporting times. Most firms, regardless their level of activity in the securities subject to this proposal, reported some trades longer than one minute from the time of execution. For agency bonds, 14.5 percent of very active reporters submitted 95 percent of their trades within one minute, compared to 13.8 percent of moderately active reporters and 35.5 percent of less-active reporters. For ABS, the percentages were 12.5 percent, 7.8 percent and 24.6 percent. For TBA, 23 percent of very active reporters took less than one minute to report 95 percent of their trades, compared to 4 percent of moderately active reporters and 11 percent of less-active reporters.

Economic impacts

Anticipated Benefits

As discussed above, FINRA is proposing to reduce the TRACE trade reporting timeframe for transactions in all TRACE-Eligible Securities that currently are subject to a 15-minute reporting timeframe. Given that 81.9 percent of the trades executed after 8:00 a.m. and before 6:15 p.m. ET were reported within one minute of execution in 2021, the proposal will result in quicker reporting and dissemination of transaction information for the remaining 4.9 million reports (or 23 trillion dollars in par value). Reducing the reporting timeframe will solidify the benefits of the technological advancements that have occurred since 2005 by requiring timelier reporting in the rule. For transactions that currently are not reported within one minute, the reporting timeframe reduction would require members to improve their current trade reporting processes to facilitate timelier reporting and allow FINRA to provide more timely pricing and other transaction information to the market, which supports price formation. Therefore, the proposal also would aid investors and other market participants in obtaining and evaluating price and other market information more quickly and act accordingly. Research has shown that TRACE dissemination improved price discovery and reduced trading costs for corporate bond investors.23 While dealers may benefit directly from the expedited price discovery, investors are also likely to benefit from fairer pricing and better executions from their dealers. The reduction in the time between trade execution and price dissemination would enhance transparency in the fixed income market and is consistent with the purpose of TRACE. Reducing the timeframe from 15 minutes to one minute will also better align the execution and dissemination framework, as there will be less variation with respect to publication versus execution time. This should make the disseminated pricing information more time relevant and therefore of greater value for market participants.

Anticipated Costs

FINRA believes that the proposal would likely result in direct and indirect costs for firms to implement changes to their processes and systems for reporting transactions to TRACE in the new timeframe. Firms that do not have automated reporting systems in place may incur costs from establishing such systems and infrastructure. Table 3 shows that, even for very active firms that most likely have a trade reporting infrastructure in place, some trades are still reported later than one minute from the time of execution. For these trades, firms may incur costs to modify their reporting procedures to report more quickly and monitor that the trades are reported in the required timeframe.

A higher percentage of less-active reporters submitted 95 percent of their trades within one minute than moderately active reporters, possibly suggesting that use of a third-party reporting system by less-active reporters may be associated with faster reporting. While members currently using a third-party reporting service may incur less costs, those that do not currently use a third-party reporting service may opt to do so if the costs would be lower than building their own system.

Request for Comment

FINRA requests comment on all aspects of the proposal. FINRA requests that commenters provide empirical data or other factual support for their comments wherever possible. In addition to general comments, FINRA specifically requests comments on the following questions:

- FINRA is proposing to reduce the trade reporting and concomitant public dissemination timeframe for corporate, agency, ABS and MBS TBA GD transactions from an outer limit of 15 minutes to one minute. FINRA acknowledges that reducing the reporting timeframe would necessitate a greater change in behavior for members in connection with some types of securities and transactions than others—e.g., ABS (see Figure 1). Do commenters agree that timelier dissemination would be beneficial for all types of TRACE-Eligible Securities that are currently subject to the 15-minute reporting timeframe?

- Would the benefits be different for different types of TRACE-Eligible Securities subject to the proposal—specifically, for corporate, agency, ABS or MBS TBA GD? In the case of corporate debt securities, would the benefits be different for investment grade than for high-yield debt?

- Would the benefits of the proposal be different for different types of market participants—e.g., retail investors, institutional investors, dealers or others? Please be specific.

- In addition to the beneficial economic impacts identified in this proposal:

- Are there other significant sources of benefits of the proposal to firms, investors or others?

- Would impacts differ for different types of investors or other market participants?

- Would impacts differ across firm size or business model?

- What would be the magnitude of these benefits?

- Do members anticipate any operational challenges in connection with complying with the proposed reporting timeframe?

- For example, do firms anticipate that reporting within one minute of execution may result in the need for additional cancellations or corrections?

- Are there specific types of products that cannot reasonably be reported within one minute of the time of execution? Please specify.

- Are there any other considerations that may complicate reporting within one minute of execution? If so, are those considerations similar for both voice and electronic executions? Please explain.

- Table 1 shows that trades with customers were reported slower than inter-dealer trades. Does the reporting process for customer trades differ from that of other types of trades in a manner that causes customer trades to be reported slower? If so, what is driving the difference in reporting? Would reducing the reporting timeframe particularly benefit transparency for customer trades? Would the proposal result in greater challenges for firms in reporting customer trades?

- Table 4 shows that only 14 percent of reports entered using the web interface were reported within one minute of trade execution. FINRA notes that reporting using the web interface is not concentrated in smaller and less active firms. Why do firms report using the web interface for certain trades? Are trades reported using the web interface different from other trades? If so, how are these trades different? How will firms currently reporting trades through the web interface change their reporting process to comply with a shortened reporting timeframe?

- Table 5 shows that 57 percent of trades executed before 8:00 a.m. or after 6:30 p.m. ET or on a non-business day were reported within one minute of the start of TRACE system hours on the next business day. Would reducing the reporting timeframe benefit the market with respect to after-hours trades? Would the proposal result in challenges for reporting after-hours trades?

- Figure 2 shows that reporting timeframes differ based on trade size, where larger trades took longer to report. Why do large trades take longer to report? Would the reduction in the reporting timeframe provide a comparatively greater benefit to the market with respect to large trades? Might the reduced timeframe result in increased costs for large trades and, if so, might these costs be passed on?

- How might the proposal affect the overall market for large trades and liquidity? For example, could faster reporting and dissemination alter incentives for dealers? Please be specific.

- How might the reduced reporting timeframe affect competition among reporters of different activity levels in TRACE-Eligible Securities? Table 3 shows that very active reporters submitted trade reports faster than other reporters. Might members’ compliance costs (e.g., costs in connection with upgrading systems) differ depending on firms’ activity levels?

- What technology, compliance or other costs would be associated with the proposed reporting timeframe reduction? Please be specific.

- How might the proposed timeframe reduction impact liquidity for corporates, agencies, ABS, and MBS TBA GD securities? Please describe.

- Are the burdens associated with requiring faster reporting for corporates, agencies, ABS and MBS TBA GD securities appropriate in light of the anticipated transparency benefits to investors and the markets.

- Should FINRA consider a longer or shorter reporting timeframe than one minute? If so, what timeframe would be appropriate, for which products, and why?

- Should FINRA consider providing any exceptions, whether on a temporary or permanent basis, for particular types of firms, for example, those with limited trading volume in corporates, agencies, ABS and MBS TBA GD securities? If so, what threshold should FINRA consider for an exception and should it differ for the different types of securities that are subject to the proposal? Are there any additional exceptions that FINRA should consider? What impacts would permitting exceptions have on the overall benefits of the proposal?

- What implementation period would be appropriate to provide members with sufficient time to comply with the proposed changes to the reporting timeframe?

- Could the proposal affect how dealers trade or otherwise change market participant behavior?

- In addition to the economic impacts identified in this proposal:

- Are there other significant sources of impacts, including direct or indirect costs of the proposed amendments to firms and investors?

- What are these economic impacts and what factors contribute to them?

- What would be the magnitude of these costs?

- Would economic impacts differ for different types of investors or other market participants?

- Would economic impacts differ across firm size or business model?

Please provide data or other supporting evidence.

- As discussed above, the proposal is limited to reducing the outer limit timeframe for reporting transactions in specific types of TRACE-Eligible Securities. FINRA continues to consider the TRACE reporting framework more broadly, including whether any additional changes may be appropriate. FINRA welcomes commenter views on further enhancements to the TRACE reporting and dissemination regime that would improve post-trade transparency for TRACE-Eligible Securities.

Endnotes

1Parties should submit in their comments only personally identifiable information, such as phone numbers and addresses, that they wish to make available publicly. FINRA, however, reserves the right to redact, remove or decline to post comments that are inappropriate for publication, such as vulgar, abusive or potentially fraudulent comment letters. FINRA also reserves the right to redact or edit personally identifiable information from comment submissions.

2See SEA Section 19 and rules thereunder. After a proposed rule change is filed with the SEC, the proposed rule change generally is published for public comment in the Federal Register. Some proposed rule changes take effect immediately upon filing with the SEC. See SEA Section 19(b)(3) and SEA Rule 19b-4.

3See Securities Exchange Act Release No. 43873 (January 23, 2001), 66 FR 8131 (January 29, 2001), (Order Approving File No. SR-NASD-99-65).

4See Securities Exchange Act Release No. 94365 (March 4, 2022), 87 FR 13781 (March 10, 2022) (Order Approving File No. SR FINRA 2021-030).

5See Gary Gensler, The Name’s Bond: Remarks at City Week (April 26, 2022).

6See FINRA Rule 6710. “TRACE-Eligible Security” means a debt security that is United States (U.S.) dollar-denominated and is: (1) issued by a U.S. or foreign private issuer, and, if a “restricted security” as defined in Securities Act Rule 144(a)(3), sold pursuant to Securities Act Rule 144A; (2) issued or guaranteed by an Agency as defined in paragraph (k) or a Government-Sponsored Enterprise as defined in paragraph (n); or (3) a U.S. Treasury Security as defined in paragraph (p). “TRACE-Eligible Security” does not include a debt security that is issued by a foreign sovereign or a Money Market Instrument as defined in paragraph (o).

7“Agency Debt Security” means a debt security that is (i) issued or guaranteed by an “agency,” as defined in Rule 6710(k); (ii) issued or guaranteed by a “government-sponsored enterprise” (GSE), as defined in Rule 6710(n); or (iii) issued by a trust or other entity that was established or sponsored by a GSE for the purpose of issuing debt securities, where such enterprise provides collateral to the trust or other entity or retains a material net economic interest in the reference tranches associated with the securities issued by the trust or other entity. The term excludes a “U.S. Treasury security,” as defined in Rule 6710(p) and a “securitized product,” as defined in Rule 6710(m), where an agency or a GSE is the “securitizer,” as defined in Rule 6710(s) (or similar person), or the guarantor of the securitized product. See FINRA Rule 6710(l).

8In 2004, FINRA (then NASD) reduced the timeframe for reporting certain TRACE-Eligible Securities, including corporate and agency debt, to within 15 minutes of the time of execution. See Securities Exchange Act Release No. 49845 (June 14, 2004), 69 FR 35088 (June 23, 2004), (Order Approving File No. SR-NASD-2004-057). See also Notice to Members 04-51 (July 2004).

9 A “List or Fixed Offering Price Transaction,” as defined in Rule 6710(q), and a “Takedown Transaction,” as defined in Rule 6710(r) are required to be reported to TRACE by the next business day (T+1). See FINRA Rule 6730(a)(2).

10“Asset-Backed Security” means a type of securitized product where the ABS is collateralized by any type of financial asset, such as a consumer or student loan, a lease, or a secured or unsecured receivable, and excludes: (i) a securitized product that is backed by residential or commercial mortgage loans, mortgage-backed securities, or other financial assets derivative of mortgage-backed securities; (ii) an “SBA-Backed ABS,” as defined in Rule 6710(bb) traded TBA as defined in Rule 6710(u) or in a “Specified Pool Transaction,” as defined in Rule 6710(x); and (iii) a collateralized debt obligation. See Rule 6710(cc).

11 “Agency Pass-Through Mortgage-Backed Security” means a type of securitized product issued in conformity with a program of an “agency,” as defined in Rule 6710(k) or a GSE as defined in Rule 6710(n), for which the timely payment of principal and interest is guaranteed by the agency or GSE, representing ownership interest in a pool (or pools) of mortgage loans structured to “pass through” the principal and interest payments to the holders of the security on a pro rata basis. See FINRA Rule 6710(v). “To Be Announced” means a transaction in an Agency Pass-Through MBS as defined in Rule 6710(v) or an SBA-Backed ABS as defined in Rule 6710(bb) where the parties agree that the seller will deliver to the buyer a pool or pool(s) of a specified face amount and meeting certain other criteria but the specific pool or pool(s) to be delivered at settlement is not specified at the time of execution, and includes TBA transactions GD and TBA transactions “not for good delivery.” See FINRA Rule 6710(u).

12In 2015, the SEC approved amendments to FINRA rules to require firms to report transactions in TRACE-Eligible Securities as soon as practicable. Securities Exchange Act Release No. 75782 (August 28, 2015), 80 FR 53375 (September 3, 2015) (Order Approving File No. SR FINRA 2015-025).

13The analysis of TRACE data contained in this Regulatory Notice is limited to transactions in TRACE-Eligible Securities that are corporates, agencies, ABS and TBA GD during the 2021 calendar year, any subsets thereof as further specified throughout.

14Table 3 shows that less active dealers reported at least some material portion of their trades within one minute, and most firms reported some material portion of their trades after one minute.

15FINRA oversees and enforces member compliance with the TRACE trade reporting rules, including regarding the timeliness of member reporting. Compliance rates with the 15-minute reporting obligation are consistently high—for example, 99.35 percent of trade reports for corporate bond transactions are received within 15 minutes.

16This group includes both reports submitted by a member that identifies an ATS as its counterparty as well as reports where a member identifies the trade as having occurred on an ATS pursuant to Rule 6732. Under Rule 6732, FINRA may grant an ATS an exemption from TRACE reporting obligations. An exempted trade occurring on the ATS must be reported by a member (other than the ATS) identifying a counterparty other than the ATS and must include the ATS’s unique MPID.

17The “non-investment grade” category above includes unrated bonds.

18Rule 144A issuances offer an opportunity for firms to quickly raise funds without the need to register securities at issuance and meet U.S. disclosure standards. 144A bonds are primarily traded by institutional investors.

19FINRA provides several alternative interfaces for TRACE reporting. TRACE supports interactive messaging via FIX protocol and a web interface (the TRACE Reporting and Quotation Service or TRAQS). TRAQS provides participants the ability to enter trades using a web browser; either one at a time or up to 50 at a time with the multi-entry functionality. See Trade Reporting and Compliance Engine (TRACE) Documentation.

20For Group 2, FINRA measured whether the trade report was submitted to TRACE within a specified number of minutes after the TRACE System opened the next business day.

21For Group 3, FINRA measured whether the trade report was submitted to TRACE within a specified number of minutes after the TRACE System opened the next business day.

22Out of 23,570,935 initial reports, 275,567 were later canceled or corrected and 23,295,368 were not. Out of the reports that were later canceled or corrected, 66 percent were reported in the first minute. Out of the reports that were not later canceled or corrected, 82 percent were reported in the first minute. The error rate for reports submitted in the first minute was 275,567 * 66 percent / (275,567 * 66 percent + 23,295,368 * 82 percent) = 0.94 percent. The error rate for reports submitted after one minute was 275,567 * 34 percent / (275,567 * 34 percent + 23,295,368 * 18 percent) = 2.3 percent.

23Hendrik Bessembinder, William Maxwell, & Kumar Venkataraman, Market transparency, liquidity externalities, and institutional trading costs in corporate bonds, 82(2) Journal of Financial Economics 251-288 (2006); Amy K. Edwards, Lawrence E. Harris, & Michael S. Piwowar, Corporate bond market transaction costs and transparency, 62(3) The Journal of Finance 1421-1451 (2007); and Michael A. Goldstein, Edith S. Hotchkiss, and Erik R. Sirri “Transparency and liquidity: A controlled experiment on corporate bonds” The Review of Financial Studies 20, no. 2 (2007): 235-273. In the municipal bond market, research has shown that customer trade costs measured as effective spread decreased after the 2005 change in the trade reporting time requirement from the end of a trading day to 15 minutes after execution. No similar studies were done in the corporate bond market, possibly due to the fact that the previous reporting timeframe reduction for corporate bonds coincided with other TRACE rule changes, so the effect was difficult to isolate. See Erick Sirri, Report on Secondary Market Trading in the Municipal Securities Market, July 14 (Research Paper, Municipal Securities Rulemaking Board); John Chalmers, Yu (Steve) Liu, & Z. Jay Wang, The Differences a Day Makes: Timely Disclosure and Trading Efficiency in the Muni Market, 139(1) Journal of Financial Economics 313-335 (2021).

| Date | Commenter |

|---|---|

| Matt Lynch Comment On Regulatory Notice 22-17 | |

| John Isaak Comment on Notice 22-17 | |

| Michael Moise Comment On Regulatory Notice 22-17 | |

| Paul Kienbaum Comment On Regulatory Notice 22-17 | |

| Healthy Markets Association Comment On Regulatory Notice 22-17 | |

| Gary Purpura Comment On Regulatory Notice 22-17 | |

| Leslie Seinfeld Comment On Regulatory Notice 22-17 | |

| Eduardo Tovar Comment On Regulatory Notice 22-17 | |

| Juan I. Sosa Comment On Regulatory Notice 22-17 | |

| Carlos Barrientos Comment On Regulatory Notice 22-17 | |

| Hartfield Titus & Donnelly LLC Comment On Regulatory Notice 22-17 | |

| Anonymous Comment On Regulatory Notice 22-17 | |

| James David Coker Comment On Regulatory Notice 22-17 | |

| Wiley Bros.-Aintree Capital Comment On Regulatory Notice 22-17 | |

| ICE Bonds Securities Corporation Comment On Regulatory Notice 22-17 | |

| Riggin Dapena Comment On Regulatory Notice 22-17 | |

| Dimensional Fund Advisors LP Comment On Regulatory Notice 22-17 | |

| TRADEliance, LLC Comment On Regulatory Notice 22-17 | |

| American Securities Association Comment On Regulatory Notice 22-17 | |

| NatAlliance Securities, LLC Comment On Regulatory Notice 22-17 | |

| Valley Financial Management, Inc. Comment On Regulatory Notice 22-17 | |

| Institutional Securities Corporation Comment On Regulatory Notice 22-17 | |

| Colliers Securities LLC Comment On Regulatory Notice 22-17 | |

| Beech Hill Securities Comment On Regulatory Notice 22-17 | |

| Financial Information Forum Comment On Regulatory Notice 22-17 | |

| Crescent Securities Group, Inc. Comment On Regulatory Notice 22-17 | |

| FIA Principal Traders Group Comment On Regulatory Notice 22-17 | |

| Seaport Global Securities, LLC Comment On Regulatory Notice 22-17 | |

| Falcon Square Capital, LLC Comment On Regulatory Notice 22-17 | |

| SAMCO Capital Markets, Inc. Comment On Regulatory Notice 22-17 | |

| Investment Company Institute Comment On Regulatory Notice 22-17 | |

| Cambridge Investment Research, Inc. Comment On Regulatory Notice 22-17 | |

| InspereX LLC Comment On Regulatory Notice 22-17 | |

| The University of Pittsburgh Securities Arbitration Clinic Comment On Regulatory Notice 22-17 | |

| BMO Capital Markets Comment On Regulatory Notice 22-17 | |

| Herbert J. Sims & Co., Inc. Comment On Regulatory Notice 22-17 | |

| SIFMA Comment On Regulatory Notice 22-17 | |

| BetaNXT Comment On Regulatory Notice 22-17 | |

| Regional Brokers, Inc. Comment On Regulatory Notice 22-17 | |

| Bond Dealers of America Comment On Regulatory Notice 22-17 | |

| Wells Fargo & Company Comment On Regulatory Notice 22-17 | |

| Isaak Bond Investments Comment On Regulatory Notice 22-17 | |

| Wholesale Markets Brokers’ Association, Americas Comment On Regulatory Notice 22-17 | |

| Arkadios Capital Comment On Regulatory Notice 22-17 |