Proposed Amendments to FINRA Rule 2165 and Retrospective Rule Review Report

Summary

The protection of senior investors is a top priority for FINRA. In August 2019, FINRA launched a retrospective review to assess the effectiveness and efficiency of its rules and administrative processes that help protect senior investors from financial exploitation. The review indicated that FINRA’s steps to protect seniors have provided helpful and effective tools in the fight against financial exploitation, but it also suggested some additional tools, guidance and rule changes.

Based on feedback received during the review, FINRA is proposing amendments to Rule 2165 (Financial Exploitation of Specified Adults) to extend the hold period and to allow temporary holds on securities transactions to further address suspected financial exploitation of senior investors. This Notice seeks comment on the proposed amendments to Rule 2165. This Notice also summarizes the retrospective rule review process, including the predominant themes that emerged from stakeholder feedback and resulting actions, and provides guidance to aid member firms and senior investors.

The proposed rule text is available in Attachment A.

Questions regarding this Notice should be directed to:

- James S. Wrona, Vice President and Associate General Counsel, Office of General Counsel (OGC), at (202) 728-8270; or

- Jeanette Wingler, Associate General Counsel, OGC, at (202) 728-8013.

Questions concerning the Economic Impact Assessment in this Notice should be directed to:

- Lori Walsh, Deputy Chief Economist, Office of the Chief Economist (OCE), at (202) 728-8323; or

- Dror Y. Kenett, Economist, OCE, at (202) 728-8208.

Action Requested

FINRA encourages all interested parties to comment. Comments must be received by December 4, 2020.

Comments must be submitted through one of the following methods:

- Online using FINRA’s comment form for this Notice;

- Emailing comments to [email protected]; or

- Mailing comments in hard copy to:

Jennifer Piorko Mitchell

Office of the Corporate Secretary

FINRA

1735 K Street, NW

Washington, DC 20006-1506

To help FINRA process comments more efficiently, persons should use only one method to comment.

Important Notes: Comments received in response to Regulatory Notices will be made available to the public on the FINRA website. In general, comments will be posted as they are received.1

Before becoming effective, the proposed rule change must be filed with the Securities and Exchange Commission (SEC or Commission) pursuant to Section 19(b) of the Securities Exchange Act of 1934 (SEA or Exchange Act).2

Background & Discussion

Retrospective Review Process

The retrospective review process has two phases: the assessment phase and the action phase. During the assessment phase, FINRA evaluates whether the rule or rule set is meeting its investor protection objectives by reasonably efficient means. The subsequent action phase implements any recommendations arising from the assessment. However, not every assessment results in a rule change. The assessment may conclude that the rule or rule set remains relevant and appropriately tailored to meet its objectives. In this instance, FINRA was focused on the rules and administrative processes that help protect senior investors from financial exploitation.

To conduct this assessment, FINRA first sought comment in Regulatory Notice 19-27 (August 2019). FINRA expressly sought comment on several questions with respect to addressing financial exploitation and other circumstances of financial vulnerability for senior investors. FINRA received 22 comment letters.3

In addition, FINRA obtained input from several advisory committees comprising member firms of different sizes and business models, investor protection advocates, member firms and trade associations. FINRA also obtained the perspective of its operating departments that touch the rules and their administration. Moreover, FINRA considered examination observations and findings involving senior issues. In this regard, FINRA previously had identified as an examination priority reviewing member firms’ controls regarding FINRA Rule 2165 (Financial Exploitation of Specified Adults), to the extent firms anticipated placing temporary holds on disbursements pursuant to the rule’s safe harbor, and the trusted contact-related amendments to Rule 4512 (Customer Account Information).4 As part of these reviews, FINRA looked at whether firms had clearly defined policies and procedures, and sought information about firms’ early experiences with these provisions.5

Finally, FINRA developed an anonymous survey that was distributed to all member firms in the first quarter of 2020. The purpose of the survey was to collect information in order to validate the feedback FINRA received and to provide an additional opportunity for all members to provide their views.6 There were 238 firms that responded to the survey, and the breakdown of these firm survey respondents according to firm size, as measured by the number of registered representatives, is provided in Table 1 below.

| Firm Size | #RRs | Industry | Survey Respondents | ||

|---|---|---|---|---|---|

| Count | %Total | Count | % Total | ||

|

Small |

1-150 | 3,153 | 90% | 141 | 59% |

| Mid-Size | 151-499 | 198 | 5% | 12 | 5% |

| Large | 500+ | 168 | 5% | 24 | 10% |

| Unknown | 0 | 0 | 0% | 61 | 26% |

| Total | 3,516 | 100 | 238 | 100% | |

Table 1: The table compares the number and percentage of firms that responded to the survey, by firm size as measured by the number of registered representatives with the total number and percentage of firms within those size categories across the industry. Survey respondents that did not provide information on the number of registered representatives in their firms were classified into the “Unknown” category.

Proposed Amendments to Rule 2165

Rule 2165 is the first uniform national standard for placing temporary holds on disbursements to address suspected financial exploitation.7 Rule 2165 permits a member firm to place a temporary hold on a disbursement of funds or securities from the account of a “specified adult”7 customer when the firm reasonably believes that financial exploitation of that adult has occurred, is occurring, has been attempted or will be attempted. Prior to the adoption of Rule 2165, some member firms expressed concern that placing a temporary hold on suspicious disbursements was not explicitly permitted by FINRA rules. To address these concerns, Rule 2165 provides member firms and their associated persons with a safe harbor from FINRA Rules 2010 (Standards of Commercial Honor and Principles of Trade), 2150 (Improper Use of Customers’ Securities or Funds; Prohibition Against Guarantees and Sharing in Accounts) and 11870 (Customer Account Transfer Contracts) when member firms exercise discretion in placing temporary holds on disbursements of funds or securities from the accounts of specified adults consistent with the requirements of Rule 2165.

Rule 2165 also includes important safeguards for customers to help ensure that there is not a misapplication of the rule, such as the requirements that: (1) a member firm provide notification of the hold and the reason for the hold to all parties authorized to transact business on the account, including the customer and the customer’s trusted contact person, no later than two business days after the date that the member first placed the hold;8 (2) a member firm relying on the rule develop and document training policies or programs reasonably designed to ensure that associated persons comply with the requirements of the rule;9 and (3) any request for a hold be escalated to a supervisor, compliance department or legal department rather than allowing an associated person handling an account to independently place a hold. Importantly, a temporary hold pursuant to Rule 2165 may be placed on a particular suspicious disbursement(s) but not on non-suspicious disbursements (e.g., a regular mortgage payment). Although FINRA encourages members to take advantage of the Rule 2165 safe harbor where there is a reasonable belief of financial exploitation, FINRA would pursue disciplinary action against a firm that uses Rule 2165 for inappropriate purposes (e.g., where a firm improperly holds a disbursement simply to prevent a customer from transferring assets to another firm rather than to prevent financial exploitation).

Temporary holds on disbursements have played a critical role in providing member firms a way to quickly respond to suspicions of financial exploitation before potentially ruinous losses occur for the customer. For example, FINRA’s report for the five-year anniversary of the FINRA Securities Helpline for Seniors® (Helpline)10 highlights several matters that illustrate the positive impact of placing temporary holds on disbursements to address financial exploitation. The matters include temporary holds placed by member firms to prevent senior investors from losing:

- $200,000 (representing approximately two-thirds of the investor’s account) related to a Central Intelligence Agency (CIA) lawsuit scam;

- $10,000 in a lottery scam;

- $60,000 in a romance scam; and

- $50,000 to financial exploitation by a brother-in-law.

The retrospective review indicated that Rule 2165 has been an effective tool in the fight against financial exploitation,11 but supported amendments to extend the hold period and to allow temporary holds on transactions to further address suspected financial exploitation of senior investors.

Hold Period

Rule 2165 allows a member firm to place a temporary hold on a specified adult customer’s account for up to 25 business days if the criteria in the rule are satisfied. The rule also provides that this period may be terminated or extended by a state agency or a court of competent jurisdiction. Stakeholders generally supported extending the current 25-business day hold period to provide member firms with a longer period to resolve matters. Stakeholders indicated that the current period may not be sufficient when a matter is under consideration by a state agency or court. This view was shared by NAPSA and the Philadelphia Financial Exploitation Task Force, which both stated that adult protective services (APS) agencies, state regulators and law enforcement typically need more time to conduct thorough investigations. In contrast, NASAA supported retaining the current 25-business day period, which aligns with the hold period provided in the NASAA Model Act to Protect Vulnerable Adults from Financial Exploitation (NASAA Model Act).

During exams in 2019 focusing on Rule 2165, member firms expressed to FINRA the need for additional time to conduct investigations and resolve matters.13 Member firms were asked in the survey distributed to member firms about possible impediments to resolving a matter within the current 25-business day hold period provided by Rule 2165. Approximately 53 percent of survey respondents stated that they had been unable to resolve a matter within the 25-business day period. The most common reason was that the matter was under consideration by a state agency (such as APS) or a court. Other common reasons included: (1) the customer did not respond to inquiries from the firm; or (2) the customer did not believe that he or she was being financially exploited. For matters that took longer to resolve than the 25-business day period, approximately 35 percent of survey respondents indicated that it took on average 26 – 50 days to resolve the matter and approximately 59 percent of survey respondents indicated that it took on average 51 – 100 days to resolve the matter.

FINRA recognizes that placing or extending a temporary hold on a disbursement is a serious step for a member and the affected customer. While FINRA recognizes that customers may be affected by temporary holds, the costs of financial exploitation can be devastating to customers, particularly older customers who rely on their savings and investments to pay their living expenses and who may not have the ability to offset a significant loss over time. Furthermore, FINRA believes that the rule’s safeguards help ensure that there is not a misapplication of the rule.

To provide member firms with additional time to resolve matters and for APS agencies, state regulators and law enforcement to conduct thorough investigations, FINRA is proposing amending Rule 2165 to permit extending a temporary hold for an additional 30 business days if the member firm had reported the matter to a state agency or a court of competent jurisdiction.14

Transactions in Securities

While placing a hold pursuant to Rule 2165 stops funds or securities from leaving a customer’s account, the rule currently does not apply to transactions in securities.15 Several external stakeholders recommended extending Rule 2165 to permit a member firm to place a temporary hold on a transaction in securities when the firm has a reasonable belief that the customer is being financially exploited. Even if a firm places a temporary hold on a disbursement out of the customer’s account, these stakeholders noted that executing a related transaction may result in significant financial consequences for the customer (e.g., tax consequences, surrender charges, the inability to regain access to a sold investment that has been closed to new investors).

Currently, there are 31 states with laws that allow investment advisers or broker-dealers to place some form of hold. Several stakeholders noted that while the NASAA Model Act does not extend to transactions, 16 of those 31 states (with approximately half of the U.S. population) have enacted laws permitting investment advisers and broker-dealers to place temporary holds on disbursements and transactions16 and that many member firms also use customer agreements that permit placing holds on transactions and disbursements.

During exams in 2019 focusing on Rule 2165, FINRA observed that some member firms included in their customer agreements the ability to place holds on transactions in securities, as well as disbursements of funds or securities, when financial exploitation is suspected. Approximately 25 percent of survey respondents indicated that their customer agreements currently permit placing temporary holds on transactions when financial exploitation is suspected.

While some state laws and customer agreements permit placing holds on transactions, FINRA is proposing to amend Rule 2165 to create the first uniform, national standard for placing holds on transactions related to suspected financial exploitation. Under the safe harbor approach, a firm would be permitted, but not required, to place a temporary hold on a transaction when there is a reasonable belief that the customer is being financially exploited.

FINRA recognizes that placing a temporary hold on a transaction is a serious step for a member and the affected customer. But FINRA also recognizes that placing a temporary hold on the underlying transaction may prevent significant negative financial consequences for the customer. These negative financial consequences can result even if a firm places a temporary hold on any related disbursement of funds out of the customer’s account. Moreover, the rule would include safeguards to protect customers and avoid misapplication of the rule, such as written supervisory procedures reasonably designed to achieve compliance with the rule, including procedures on the identification, escalation and reporting of matters related to financial exploitation of specified adults.17

Economic Impact of the Proposal

FINRA has undertaken an economic impact assessment, as set forth below, to further analyze the regulatory need for the proposed rule change, its potential economic impacts, including anticipated costs, benefits, and distributional and competitive effects relative to the current baseline, and the alternatives FINRA considered in assessing how best to meet its regulatory objective.

Regulatory Need

FINRA is active in its efforts to protect senior investors from financial exploitation. In the context of these efforts, and with evidence of a growing trend of such exploitation, FINRA conducted a review of relevant existing rules and administrative processes that help protect senior investors from financial exploitation. Through this review, FINRA has received feedback on the effectiveness and efficiency of Rule 2165.

Economic Baseline

The economic baseline for the proposed rule amendments is the current Rule 2165 and its use by member firms, as well as existing firm policies and state laws related to protecting senior investors. To conduct the assessment phase of the retrospective rule review, FINRA first sought comment in Regulatory Notice 19-27. FINRA obtained input from several advisory committees comprising member firms of different sizes and business models, investor protection advocates, and member firms, and from trade associations. In addition, FINRA obtained the perspective of its operating departments that touch the rules and their administration.

FINRA also distributed a survey to all member firms in the first quarter of 2020, to which a subset of firms, ranging from small to large firms, responded. The purpose of the survey was to collect information and to provide member firms an additional opportunity to provide their views. The economic baseline, regarding the current application of the rule by firms and the effectiveness and efficiency of the rule is established using the information obtained during the assessment phase.

As noted above, with respect to the use of Rule 2165 in placing a temporary hold on disbursements, of the member firms that indicated having placed a temporary hold,18 approximately 53 percent of survey respondents stated that the firm had been unable to resolve the matter within the 25-business day period provided by the rule. For firms responding that any matter took longer to resolve than the 25-business day period, approximately 35 percent indicated that it took on average 26 – 50 days to resolve the matter and approximately 59 percent indicated that it took on average 51 – 100 days to resolve the matter.

With respect to the issue of placing a temporary hold on transactions, approximately 25 percent of firm respondents to the survey indicated that their customer agreements currently permit placing temporary holds on transactions. Of these, 22 firms reported that they had placed a temporary hold pursuant to the customer agreement.19 The majority of these 22 firms have done so no more than 10 times a year, on average. In addition, currently 16 states (with approximately half of the U.S. population) have enacted laws permitting investment advisers and broker-dealers to place temporary holds on disbursements and transactions.

Economic Impacts

FINRA has analyzed the potential costs and benefits of the proposed amendments, and the different parties that are expected to be affected. FINRA has identified senior investors and member firms that serve senior investors as the main parties to be impacted by the proposed amendments.

The proposed amendments to Rule 2165 would permit extending a temporary hold for an additional 30 business days if the member firm had reported the matter to a state agency or a court of competent jurisdiction. FINRA believes that allowing for an extension to the temporary hold period would allow for additional time for firms to resolve matters and for APS agencies, state regulators and law enforcement to conduct thorough investigations of suspected financial exploitation. Moreover, extensions may allow for greater collaboration and interaction with other authorities or regulators on a local, state or national level. Customers would benefit from this extension in instances where the additional time allows for a positive identification of financial exploitation and retention of the disbursement amount within the account. Alternatively, if the additional time leads to a determination that no financial exploitation occurred, customers may incur costs from the extended delay in access to the funds.

The proposed amendments would also extend Rule 2165 to permit a member firm to place a temporary hold on a transaction in securities when the firm has a reasonable belief that the customer is being financially exploited. Sixteen states, together containing approximately half of the US population, already permit firms to place temporary holds on transactions. Thus, the proposed amendments would impact firms not located in a state that already permits it but that decide to take advantage of the proposed extension of Rule 2165 holds to transactions.20 The proposed amendments would also impact the customers of those firms. In instances when a firm’s hold on a transaction prevented financial exploitation, the customer whose transaction was held would benefit from not incurring the negative financial consequences of the transaction. In instances when a transaction hold was placed and no financial exploitation was found, the economic impact of the hold stems primarily from the magnitude of the security’s price movement (positive or negative) between the time the hold was placed and the time it was lifted.

Alternatives Considered

FINRA considered various alternatives to the proposed rule amendments. First, FINRA considered proposing different hold period extensions, ranging from no extension to an extension of up to 75 business days. FINRA also considered not extending Rule 2165 to transactions, but rather keeping the temporary hold option only for disbursements. Ultimately, FINRA has found the proposed amendments to strike an appropriate balance between regulatory burden, investor protection and investor choice.

Other Key Themes From the Assessment

Addressing Financial Exploitation

Stakeholders indicated the prevalence of and problems associated with financial exploitation of senior investors, including longstanding harm to customers. Several commenters to Regulatory Notice 19-27 stated that the Helpline,21 educational materials prepared and distributed by FINRA, Rule 2165 and the trusted contact amendments to Rule 4512 have been helpful and effective tools in the fight against financial exploitation.

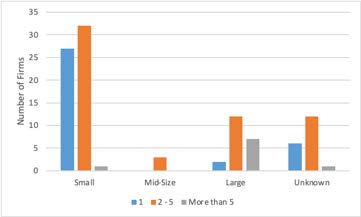

The retrospective review indicated that some member firms have a dedicated person or team to handle senior investor issues. Based on information collected in the survey, these member firms most commonly dedicated two to five firm staff to handling senior investor issues (see Figure 1 for breakdown by firm size).

Figure 1: Number of firms with full time equivalent (FTE) staff dedicated to senior investor issues, with 1 FTE, 2 – 5 FTE, and more than 5 FTE, broken down by firm size. Approximately half of respondents indicated a dedicated staff of 2 – 5 FTE. Of the 238 firms that responded to the survey, only 105 firms answered yes to whether they have staff dedicated to senior investor issues, and of those 103 firms provided the information regarding number of FTE.

Rule 2165 Notification Period

Rule 2165 requires the member to provide notification of the hold and the reason for the hold to the trusted contact person and all parties authorized to transact business on the account, including, but not limited to, the customer, no later than two business days after the date that the member first placed the hold.22 Some external stakeholders suggested flexibility around the two-day notification period to the trusted contact person when the member firm needs time to investigate whether the trusted contact person may be involved in the exploitation. In response, in March 2020, FINRA published a set of frequently asked questions (FAQ) providing that a member firm may refrain from providing notification to an authorized party or the trusted contact person if the firm reasonably suspects that the authorized party or trusted contact person, respectively, may be engaged in the financial exploitation but needs additional time to conduct an investigation. If the member firm’s subsequent investigation indicates that the authorized party or trusted contact person is not engaged in the financial exploitation, the FAQ states that the member firm should provide the notification to the authorized party or the trusted contact person, respectively.23

Cognitive Decline or Diminished Capacity

Some stakeholders supported extending Rule 2165 to situations where a firm has a reasonable belief that the customer has an impairment, such as diminished capacity, that renders the individual unable to protect his or her own interests, even though there is no evidence of financial exploitation. However, other stakeholders expressed concerns that member firms are not well-positioned to determine if a customer is suffering from cognitive decline or diminished capacity in the absence of suspected financial exploitation. In addition, the Cornell Clinic, NASAA, PIABA and Pittsburgh Clinic expressed concerns that such an extension would give member firms too much discretion or would unfairly impede customer autonomy.

FINRA is not proposing to extend Rule 2165 to situations where a member firm has a reasonable belief that the customer has cognitive decline or diminished capacity but there is no evidence of financial exploitation. Rather than rulemaking, FINRA is summarizing the information obtained about member firms’ procedures and practices in this area in this Notice to assist other member firms and investors.

FINRA included questions in the survey to member firms to better understand member firms’ procedures and practices regarding addressing suspected customer cognitive decline or diminished capacity. Approximately 52 percent reported having specific procedures in this area, including procedures related to:

- training to identify red flags of customer cognitive decline or diminished capacity;

- the use of targeted, successful methods to obtain information on a trusted contact person, discussed in more detail below;

- documenting and escalating suspected customer cognitive decline or diminished capacity to a specific person, office or team for review and response;

- contacting a trusted contact person or another authorized party;

- suggesting that the customer be seen by a medical professional;

- additional supervision of related customer accounts; and

- reporting matters to APS or law enforcement.

Some member firms also indicated that their customer agreements provide that the firm may place a temporary hold on transactions in securities or disbursements of funds or securities when the firm suspects a customer is suffering from cognitive decline or diminished capacity.

Red flags of diminished capacity or cognitive decline, may include:

- confusion;

- memory loss;

- disorientation with surroundings or during social interactions;

- difficulty speaking or communicating;

- poor judgment or the inability to appreciate the consequences of decisions;

- sudden and unexplained changes to risk tolerance or investment methodology, including increased risk taking;

- difficulty contacting the customer;

- repeated calls or requests for the same information;

- uncharacteristic changes in appearance, demeanor or behavior; or

- drastic mood swings or irritability.

Reporting Requirements

FINRA Rule 4530 (Reporting Requirements) requires member firms to report specified events to FINRA. For some situations, FINRA has developed problem codes for use in reporting pursuant to FINRA Rule 4530 to provide clarity regarding the reportable event. To date, FINRA has not developed a dedicated problem code for Rule 2165-related reporting. In addition, Form U4 (Uniform Application for Securities Industry Registration or Transfer), which member firms use to register associated persons with FINRA and the appropriate jurisdictions, and Form U5 (Uniform Termination Notice for Securities Industry Registration), which member firms use to terminate the registration of associated persons with FINRA and the appropriate jurisdictions, require disclosing customer complaints that meet specified criteria. Rule 4530 and Forms U4 and U5 have different thresholds and analysis for whether a complaint is reportable. In general, FINRA uses complaints reported pursuant to Rule 4530 for regulatory purposes but does not make these complaints public, while complaints reported pursuant to Forms U4 and U5 are public facing. In addition, while Rule 4530 is a FINRA rule, the SEC, self-regulatory organizations, the states and other governmental jurisdictions use Forms U4 and U5. Any amendments to or guidance on Forms U4 and U5 would be subject to discussion with these users.

Several external stakeholders expressed concern that Rule 2165’s safe harbor does not extend to complaints reportable on Forms U4 or U5 or pursuant to Rule 4530 about an associated person whose actions were within the safe harbor and stated that some member firms and associated persons may choose not to place a hold pursuant to Rule 2165 because of concerns about a possible customer complaint. Some of these external stakeholders requested guidance on when a Rule 2165-related complaint would be reportable and supported developing a specific problem code for reporting any Rule 2165-related complaint to FINRA pursuant to FINRA Rule 4530. In contrast, NASAA stated in its comment letter to Regulatory Notice 19-27 that to the extent that a complaint meets the criteria to be reported on Forms U4 or U5, it should be reported on the uniform forms.24

To date, based on FINRA’s review of reported complaints, member firms have not reported a complaint on Forms U4 or U5 or pursuant to Rule 4530 related to placing a temporary hold pursuant to Rule 2165. Moreover, survey respondents indicated that they had not reported a complaint on Form U4 or Form U5 or pursuant to Rule 4530 related to placing any temporary holds.

Rule 2165’s safe harbor does not extend to complaint reporting because, among other things, FINRA rules do not limit a customer’s right to submit a complaint about an associated person related to any statute, regulation or rule. However, any complaint would be reportable only if it met the specified criteria for reporting in Forms U4 or U5 or Rule 4530. Moreover, FINRA would consider whether a member or associated person had acted consistent with Rule 2165 when assessing any reported information about a hold.

FINRA does not currently plan to propose guidance regarding when a Rule 2165-related complaint would be reportable or develop a specific problem code for reporting any Rule 2165-related complaint to FINRA pursuant to FINRA Rule 4530. In considering whether a complaint is reportable, member firms should use the existing publicly available guidance. FINRA may reconsider this issue or develop a specified problem code for reporting any Rule 2165-related complaint to FINRA pursuant to FINRA Rule 4530 if complaints are reported in the future and they appear to have a detrimental impact on the protection of seniors and other vulnerable adults.

FINRA Rule 4512

Rule 4512 requires member firms to make reasonable efforts to obtain the name of and contact information for a trusted contact person upon the opening of a non-institutional customer’s account or when updating account information for a non-institutional account in existence prior to the effective date of the amendments (existing account). The trusted contact person is intended to be a resource for the member in administering the customer’s account, protecting assets and responding to possible financial exploitation. Member firms are not prohibited from opening and maintaining an account if a customer fails to identify a trusted contact person provided the member firm makes reasonable efforts to obtain the information.

Stakeholders expressed the benefits of discussions with customers about adding a trusted contact person. For example, Lara May and SIFMA indicated in their comment letters to Regulatory Notice 19-27 that requesting that customers name trusted contact persons had been an opportunity to engage in beneficial conversations about scams to help insulate customers against financial exploitation. Moreover, external stakeholders expressed the benefit of being able to contact an available trusted contact person in administering a customer’s account (e.g., where customers had recently changed phone numbers or moved without updating their contact information; where customers were on extended trips; and where firms had concerns over customers’ possible diminished capacity even though there was no indication of financial exploitation). External stakeholders also noted that some member firms permit customers to name more than one trusted contact person and that this may be helpful, for example, where a customer would like to name multiple children as trusted contact persons.

If a customer has not named a trusted contact person or the trusted contact person may be otherwise unavailable, survey respondents indicated that they have reached out to another authorized party, such as a joint accountholder, power of attorney, legal counsel or accountant. Survey respondents also reported that they may ask the customer if another party (e.g., a spouse or adult child) can attend meetings discussing the customer’s account.

Methods

Because external stakeholders expressed concern with customer response rates, FINRA sought information in the survey to member firms on percentages of existing and new customers and who had provided information for a trusted person contact as of the first quarter of 2020. Most survey respondents indicated that 25 percent or less of the firm’s existing or new customers had provided trusted contact information. In addition, member firms were asked about methods they used to seek the name and contact information for a trusted contact person and customer response rates. Survey respondents indicated that they had the best response rates when seeking the trusted contact person information:

- in the account opening agreement;

- during one-on-one conversations between a financial professional and the customer; and

- with a prompt when the customer calls.

Member firms may find it helpful to incorporate these methods as part of seeking the name and contact information for a trusted contact person.

Customer Education

External stakeholders also shared that some customers incorrectly believe that naming a trusted contact person would give that person authority over the customer’s account. Because many people believe that they could never be the victim of financial exploitation, internal and external stakeholders also suggested highlighting that the trusted contact person can be used in a broader range of situations pursuant to Rule 4512 (e.g., if the member firm has been unable to contact the customer after multiple attempts). To that end, SEC’s Office of Investor Education and Advocacy and FINRA collaborated on an Investor Bulletin that helps customers understand the purpose of designating a trusted contact person for brokerage accounts, and encourages customers to designate a trusted contact person. The Investor Bulletin was published in March 2020 and is available on the SEC’s website and on FINRA’s website. Member firms may find it helpful to use in communicating with customers. In addition, in April 2018, FINRA published a similar article providing information on the trusted contact person-related amendments to Rule 4512 and Rule 2165 for investors and member firms and made a downloadable print version available.

Sanction Guidelines

Internal and external stakeholders supported amending FINRA's Sanction Guidelines to include as a principal consideration when assessing appropriate sanctions the customer's age or physical or mental impairments. The National Adjudicatory Council (NAC) approved amendments to the Principal Considerations in Determining Sanction section of the Sanction Guidelines to expressly contemplate the customer’s age or physical or mental impairment that renders the individual unable to protect his or her own interests. These amendments to the Sanction Guidelines and the effective date will be discussed in greater detail in a separate Regulatory Notice.

Marketing of Products and Strategies to Senior Investors

Some stakeholders supported heightened supervision for the marketing and sale of complex products and strategies to senior investors but expressed skepticism about the value of requiring additional disclosure for these products and strategies. Approximately 51 percent of survey respondents indicated having specific procedures related to marketing securities products and strategies to seniors, including, for example:

- events, such as lunches, geared to senior investors;

- use of senior-related designations by registered persons; and

- heightened review by a firm’s compliance department of any marketing to senior investors.25

Furthermore, approximately 16 percent of these firms reported providing additional disclosure to senior investors regarding:

- annuities;

- alternative products; and

- products as required by some states.

FINRA has previously published guidance:

- In Regulatory Notice 12-03 (January 2012) on the supervision of complex products by member firms;

- In Regulatory Notice 11-52 (November 2011) regarding the supervision of registered persons using senior designations;

- In Regulatory Notice 08-27 (May 2008) regarding supervising registered representatives' use of marketing materials to establish expertise; and

- In Regulatory Notice 07-43 (September 2007) on member firms’ obligations relating to senior investors, including best practices in making recommendations and in communicating with senior investors.

FINRA reminds member firms of this prior guidance and its applicability to the marketing and sale of complex products and strategies to senior investors.

Customer Disputes

PIABA urged FINRA to emphasize to arbitrators the importance of expeditiously resolving disputes involving senior investors. FINRA Dispute Resolution Services has provided guidance on expedited proceedings for senior or seriously ill investors.26

Information Sharing

External stakeholders requested guidance on the ability of a member firm to share information with another financial institution when it believes that a customer is the victim of financial exploitation. In response, in March 2020, FINRA published a new FAQ noting that, in many instances, a member would be permitted to disclose information to another financial institution related to suspected financial exploitation.27 The FAQ states that: (1) Regulation S-P allows a member to share nonpublic personal information with non-affiliated third parties for certain purposes, including to protect against or prevent actual or potential fraud, unauthorized transactions, claims, or other liability;28 and (2) Section 314(b) of the USA PATRIOT Act permits a financial institution, upon providing notice to the United States Department of the Treasury, to share information with other financial institutions in order to identify and report to the federal government activities that may involve money laundering or terrorist activity.29

Outreach and Collaboration

Stakeholders recommended that FINRA continue to partner with stakeholders such as the SEC, state securities regulators, state and county APS and senior-focused associations to address financial exploitation and to improve understanding of the FINRA rules in this area. FINRA has and will continue to prioritize senior investors and address financial exploitation of senior investors, including through:

- carrying out a multi-faceted investor protection campaign through the FINRA Foundation aimed at promoting awareness about, and support for, the prevention of financial fraud while simultaneously empowering financial consumers to protect themselves, using such tactics as:

- fraud prevention and victim advocate training in collaboration with federal and state securities regulators, APS groups, NAPSA, the National Center for Victims of Crime, the National White Collar Crime Center, and staff from FINRA’s National Cause and Financial Crimes Detection Programs;

- engaging in outreach—often in coordination with the SEC, state securities regulators, and nonprofits such as AARP and the Better Business Bureau—to empower financial consumers to spot, avoid, and report financial fraud;

- conducting and supporting research focused on financial exploitation and fraud as well as aging and financial decision-making, which is shared with internal and external stakeholders;30

- issuing alerts and articles educating investors about important issues and highlighting risks facing senior investors;31

- launching the dedicated Helpline—available at (844) 57-HELPS—to provide senior investors and their family members with a supportive place to get assistance from specially trained FINRA staff related to concerns they have with their brokerage accounts and investments; and

- collaborating with NASAA and the SEC to address senior investor protection, including issuing a Senior Safe Act Fact Sheet designed to raise awareness among member firms, investment advisers and transfer agents about the act and its immunity provisions.32

FINRA Rule 3240 (Borrowing From or Lending to Customers)

The retrospective review also sought stakeholders’ input on the effectiveness of Rule 3240. FINRA will summarize those views and any proposed amendments to the rule, guidance or other actions resulting from the findings in a separate Regulatory Notice.

Request for Comments on Proposed Amendments to Rule 2165

FINRA requests comment on all aspects of the proposed amendments to Rule 2165. FINRA requests that commenters provide empirical data or other factual support for their comments wherever possible. FINRA specifically requests comment concerning the following issues:

- What are the alternative approaches, other than the proposed amendments to Rule 2165, that FINRA should consider?

- Should Rule 2165’s safe harbor be extended to apply to transactions in securities, in addition to disbursements of funds and securities? What are the implications of extending the safe harbor to transactions?

- Should Rule 2165’s temporary hold period be extended as proposed?

- Has your firm identified any unintended consequences when placing or attempting to place a temporary hold on disbursement of funds or securities from an account under Rule 2165?

- Are there any material economic impacts, including costs and benefits, to investors, issuers and firms that are associated specifically with the proposal? If so:

- What are these economic impacts and what are their primary sources?

- To what extent would these economic impacts differ by business attributes, such as size of firm or differences in business models?

- What would be the magnitude of these impacts, including costs and benefits?

- Are there any expected economic impacts associated with the proposal not discussed in this Notice? What are they and what are the estimates of those impacts?

Endnotes

- Parties should submit in their comments only personally identifiable information, such as phone numbers and addresses, that they wish to make available publicly. FINRA, however, reserves the right to redact, remove or decline to post comments that are inappropriate for publication, such as vulgar, abusive or potentially fraudulent comment letters. FINRA also reserves the right to redact or edit personally identifiable information from comment submissions.

- See SEA Section 19 and rules thereunder. After a proposed rule change is filed with the SEC, the proposed rule change generally is published for public comment in the Federal Register. Certain limited types of proposed rule changes take effect upon filing with the SEC. See SEA Section 19(b)(3) and SEA Rule 19b-4.

- The comment letters were from: anonymous (February 26, 2020); Eric Arnold, Clifford Kirsch and Holly Smith of Eversheds Sutherland on behalf of the Committee of Annuity Insurers (October 8, 2019) (CAI); Seth A. Miller, General Counsel, Executive Vice President, and Chief Risk Officer, Cambridge Investment Research, Inc. (October 8, 2019) (Cambridge); William A. Jacobson, Esq., Clinical Professor of Law and Director, and Nicole A. Jaeckel, Securities Law Clinic Cornell Law School (October 7, 2019) (Cornell Clinic); Christopher Bok, Director, Financial Information Forum (October 8, 2019) (FIF); Marc Fitapelli, Esq., Fitapelli Kurta (October 8, 2019) (Fitapelli Kurta); Robin M. Traxler, Senior Vice President, Policy & Deputy General Counsel, Financial Services Institute (October 8, 2019) (FSI); Jennifer L. Szaro, Lara May & Associates, LLC, and Robert L. Hamman, President, First Asset Financial Inc. (October 4, 2019) (Lara May); Maureen K. Paparo, Lincoln Square Legal Services (October 8, 2019) (Lincoln Square); Megan Valent and Teresa J. Verges, University of Miami School of Law (October 1, 2019) (Miami Investor Rights Clinic); Courtney Rogers Reid, Lead Counsel, Broker-Dealer and Investment Adviser Practice Group, MML Investors Services, LLC (October 8, 2019) (MMLIS); Kathleen Quinn, Board President, National Adult Protective Services Association (October 8, 2019) (NAPSA); Christine Lazaro, President, and Samuel B. Edwards, Executive Vice President, Public Investors Advocate Bar Association (October 8, 2019) (PIABA); Christopher Gerold, President, North American Securities Administrators Association (October 8, 2019) (NASAA); Nancy Brown, President and Co-Chair, and Dian VanderWell, Opportunity Alliance Nevada (October 8, 2019) (Opportunity Alliance Nevada); Joe Snyder, Chair, Philadelphia Financial Exploitation Task Force (October 7, 2019) (Philadelphia Financial Exploitation Task Force); Alice L. Stewart, Director, University of Pittsburgh School of Law – Securities Arbitration Clinic (October 8, 2019) (Pittsburgh Clinic); Erin K. Lineham, Associate General Counsel – Compliance, Raymond James & Associates, Inc. (October 29, 2019) (Raymond James); Lisa J. Bleier, Managing Director, Securities Industry and Financial Markets Association (October 8, 2019) (SIFMA); Christine Lazaro, Professor of Clinical Legal Education and Director, St. John’s University School of Law Securities Arbitration Clinic (October 8, 2019) (St. John’s Clinic); and Ron Long, Head of Elder Client Initiatives Center of Excellence, Wells Fargo & Company (October 8, 2019) (Wells Fargo). In addition, we received a letter dated November 15, 2019 from SIFMA supplementing its original letter.

- See 2019 Annual Risk Monitoring and Examination Priorities Letter (Jan. 22, 2019).

- See id.

- Survey respondents were permitted to skip survey questions. Information in this Notice regarding the percentage of survey respondents for a particular question reflects the percentage of respondents for that question, not the percentage of respondents for the survey as a whole. Approximately 190 responses were received for each top-level (non-nested) question. Therefore, unless indicated otherwise, the reader can assume that the percentages are based on approximately 190 responses.

- See Securities Exchange Act Release No. 79964 (Feb. 3, 2017), 82 FR 10059 (Feb. 9, 2017) (Notice of Filing of Partial Amendment No. 1 and Order Granting Accelerated Approval of File No. SR-FINRA-2016-039) (Approval Order).

- The definition of “specified adult” in Rule 2165 covers those investors who are particularly susceptible to financial exploitation. A “specified adult” is (A) a natural person age 65 and older or (B) a natural person age 18 and older who the member reasonably believes has a mental or physical impairment that renders the individual unable to protect his or her own interests. See Rule 2165(a)(1). Supplementary Material .03 to Rule 2165 provides that a member’s reasonable belief that a natural person age 18 and older has a mental or physical impairment that renders the individual unable to protect his or her own interests may be based on the facts and circumstances observed in the member’s business relationship with the person.

- See Rule 2165(b)(1)(B).

- See Supplementary Material .02 to Rule 2165.

- See Protecting Senior Investors 2015–2020: An Update on the FINRA Securities Helpline for Seniors, Other FINRA Initiatives and Member Firm Practices.

- During exams in 2019 focusing on Rule 2165, FINRA observed that large firms were more likely than small firms to place temporary holds pursuant to Rule 2165. Some member firms that declined to use the safe harbor cited litigation risks associated with placing temporary holds or in evaluating whether a customer is being financially exploited. This is consistent with our survey responses with large firms indicating that they had placed a temporary hold pursuant to the rule in a significantly larger percentage than mid-size or small firms. Thirty-one survey respondents had placed a temporary hold pursuant to Rule 2165. Eighty-four percent of large firm respondents had placed a hold pursuant to Rule 2165, while only 6 percent of all other sized firms had placed a hold pursuant to Rule 2165.

- In 2019, FINRA identified as an examination priority: (1) reviewing member firms’ controls regarding their obligations under trusted contact person-related amendments to FINRA Rule 4512 and Rule 2165, to the extent that firms anticipate placing temporary holds on disbursements pursuant to the Rule 2165 safe harbor, including whether firms have clearly defined policies and procedures or practices; and (2) learning about firms’ early experiences with these provisions. See 2019 Annual Risk Monitoring and Examination Priorities Letter (Jan. 22, 2019).

- The 30-business day hold period in proposed Rule 2165(b)(4) would be in addition to the 15-business day hold in Rule 2165(b)(2) and the 10-business day hold in Rule 2165(b)(3).

- For example, Rule 2165 currently would not apply to a customer’s order to sell his shares of a stock. However, if a customer requested that the proceeds of a sale of shares of a stock be disbursed out of his account at the member firm, then the rule could apply to the disbursement of the proceeds where the customer is a “specified adult” and there is reasonable belief of financial exploitation.

- As of September 2020, the following states permit holds on disbursement and transactions: Arizona, California, Florida, Kentucky, Minnesota, Mississippi, Missouri, New Jersey, New Mexico, North Dakota, Oklahoma, Texas, Utah, Virginia, Washington State and West Virginia. The Oklahoma provision becomes effective in November 2020.

- See Rule 2165(c).

- Thirty-one firms responded in the survey that they had placed a temporary hold. Out of the 31 firms that indicated that they had placed a temporary hold, 17 firms indicated that it took more than the 25-business day period to resolve the matter, as currently provided in Rule 2165.

- These 22 firms represent approximately half of all firms that reported that their customer agreements permit them to place a temporary hold on transactions in a customer account.

- When asked in the survey about FINRA extending Rule 2165 to transactions, respondents were evenly split with 50 percent anticipating that the member firm would place holds on transactions pursuant to amended Rule 2165 and 50 percent anticipating that the firm would not place holds.

- Additional information about the Helpline is available on its dedicated webpage.

- See Rule 2165(b)(1)(B). FINRA understands that a member may not necessarily be able to speak with or otherwise get a response from such persons within the two-business-day period. FINRA would consider, for example, a member's mailing a letter, sending an email, or placing a telephone call and leaving a message with appropriate person(s) within the two-business-day period to constitute notification for purposes of Rule 2165.

- The FAQ was added to the existing FAQs Regarding FINRA Rules Relating to Financial Exploitation of Senior Investors.

- See Form U4 and U5 Interpretive Questions and Answers providing guidance on when a complaint is reportable on Forms U4 or U5.

- Member firms may adopt procedures regarding marketing securities products and strategies to senior investors as part of having a supervisory system reasonably designed to achieve compliance with the securities laws and FINRA rules, such as FINRA Rule 2210 (Communications with the Public).

- See Expedited Proceedings for Senior or Seriously Ill Parties.

- The FAQ was added to the existing FAQs Regarding FINRA Rules Relating to Financial Exploitation of Senior Investors.

- See 17 CFR § 248.15(a)(2)(ii).

- See 31 CFR § 1010.540 (Voluntary information sharing among financial institutions); the United States Department of the Treasury’s Financial Crimes Enforcement Network (“FinCEN”) SAR Activity Review Issue 23 (Apr. 30, 2013) (providing examples of information sharing among financial institutions pursuant to Section 314(b), including for suspected financial exploitation of a senior); and additional information from FinCEN available at https://www.fincen.gov/section-314b. See also 31 CFR § 1023.320(e) (Reports by brokers or dealers in securities of suspicious transactions) regarding the requirement to maintain the confidentiality of suspicious activity reports.

- See FINRA Investor Education Foundation and Investor Protection Campaign Research.

- See, e.g., articles such as Protecting Seniors from Financial Exploitation; Investor Alerts such as Power of Attorney and Your Investments–10 Tips, Plan for Transition: What You Should Know About the Transfer of Brokerage Account Assets on Death, and Seniors Beware: What You Should Know About Life Settlements; and FINRA’s Retirement webpage for investors.

- See http://www.finra.org/sites/default/files/senior_safe_act_factsheet.pdf.

| Date | Commenter |

|---|---|

| Wendy Norcross Comment On Regulatory Notice 20-34 | |

| University of Pittsburgh Comment On Regulatory Notice 20-34 | |

| Edward Jones Comment On Regulatory Notice 20-34 | |

| University of Miami School of Law Comment On Regulatory Notice 20-34 | |

| Leonida Manabat Comment On Regulatory Notice 20-34 | |

| Wells Fargo & Company Comment On Regulatory Notice 20-34 | |

| Cambridge Investment Research, Inc. Comment On Reg Notice 20-34 | |

| National Adult Protective Services Association Comment On Regulatory Notice 20-34 | |

| SIFMA Comment On Regulatory Notice 20-34 | |

| Philadelphia Financial Exploitation Prevention Task Force Comment On Regulatory Notice 20-34 | |

| Public Investors Advocate Bar Association Comment On Regulatory Notice 20-34 | |

| Insured Retirement Institute Comment On Regulatory Notice 20-34 | |

| Financial Services Institute Comment On Regulatory Notice 20-34 | |

| Fidelity Investment Comment On Regulatory Notice 20-34 | |

| LPL Financial Comment On Regulatory Notice 20-34 | |

| Commonwealth Financial Network Comment On Regulatory Notice 20-34 | |

| MML Investors Services, LLC (MMLIS) Comment On Regulatory Notice 20-34 | |

| Eversheds Sutherland (US) LLP for The Committee of Annuity Insurers Comment On Regulatory Notice 20-34 | |

| NASAA Comment On Regulatory Notice 20-34 |