FINRA-Registered Firms

Table of Contents

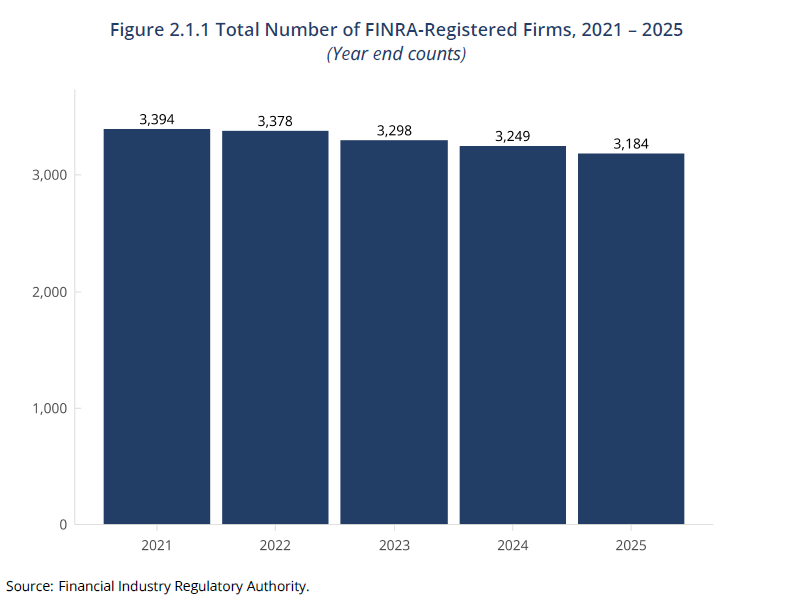

- Figure 2.1.1 Total Number of FINRA-Registered Firms, 2021−2025

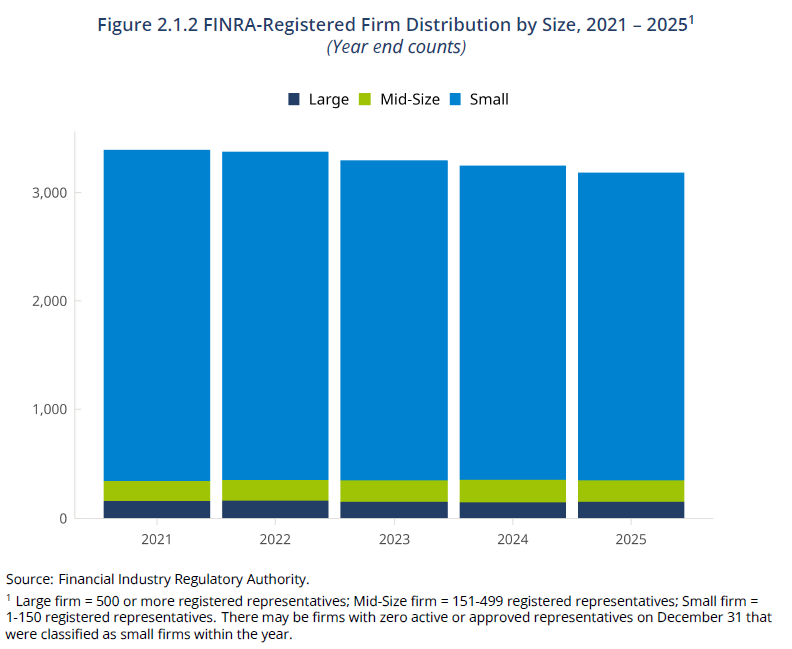

- Figure 2.1.2 FINRA-Registered Firm Distribution by Size, 2021−2025

- Table 2.1.3 FINRA-Registered Firm Distribution by Size, 2021−2025

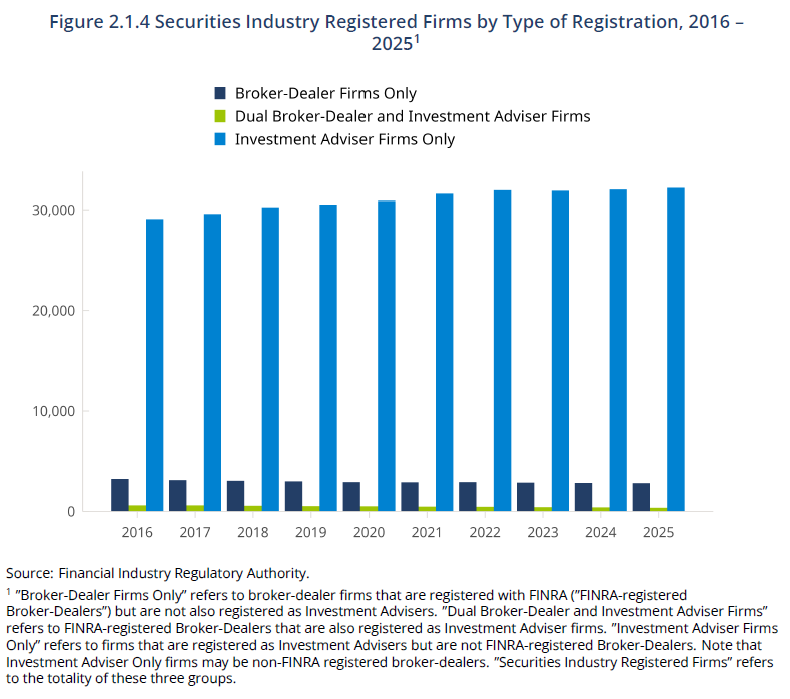

- Figure 2.1.4 Securities Industry Registered Firms by Type of Registration, 2016−2025

- Table 2.1.5 Securities Industry Registered Firms by Type of Registration, 2016−2025

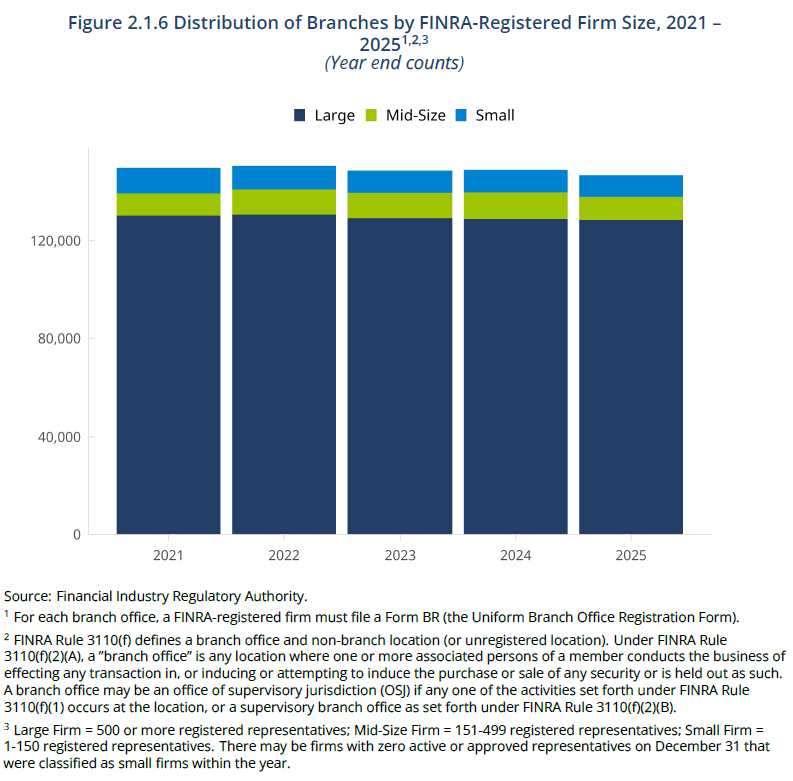

- Figure 2.1.6 Distribution of Branches by FINRA-Registered Firm Size, 2021−2025

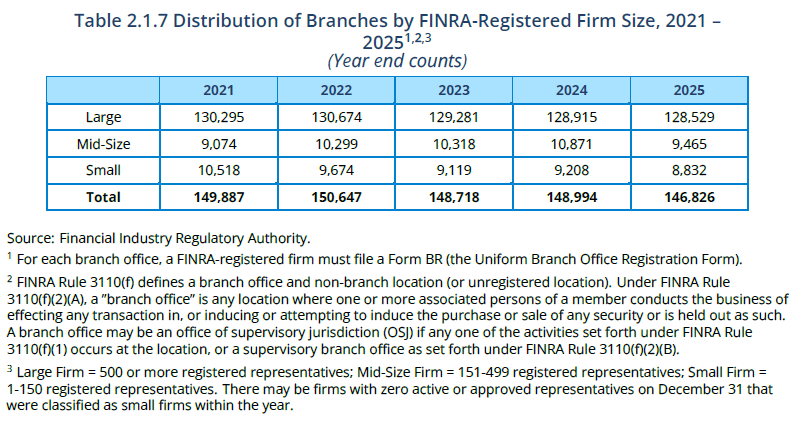

- Table 2.1.7 Distribution of Branches by FINRA-Registered Firm Size, 2021−2025

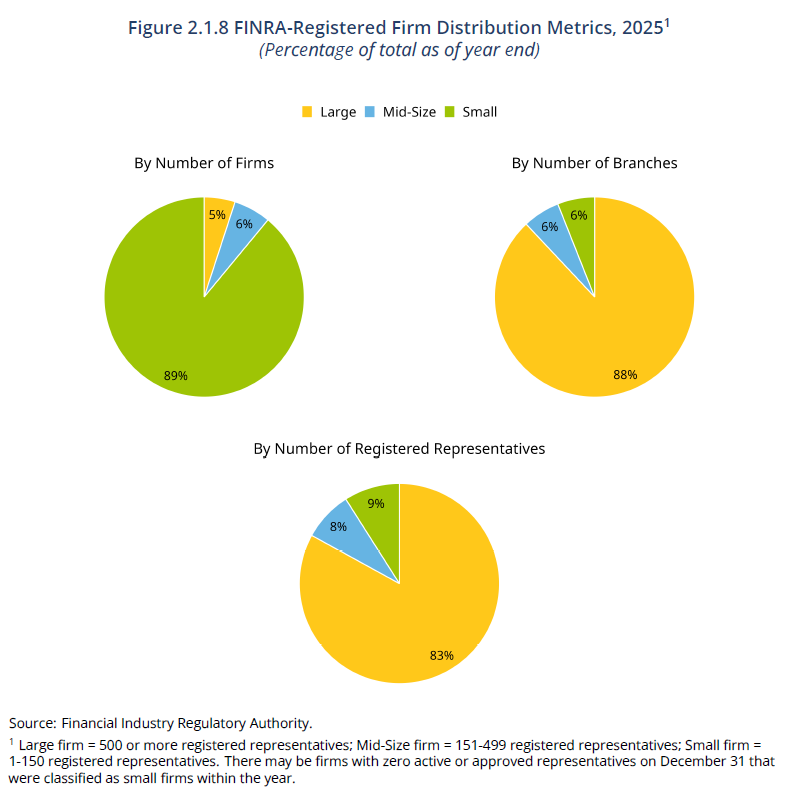

- Figure 2.1.8 FINRA-Registered Firm Distribution Metrics, 2025

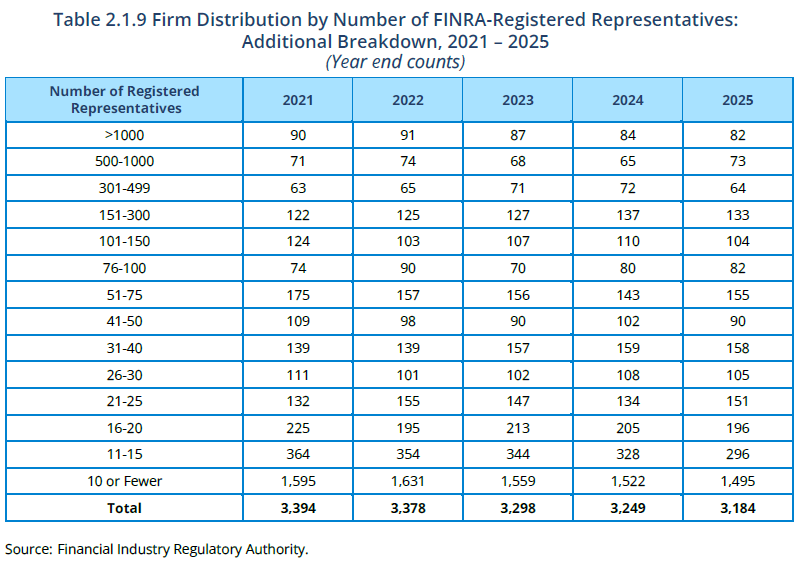

- Table 2.1.9 Firm Distribution by Number of FINRA-Registered Representatives: Additional Breakdown, 2021–2025

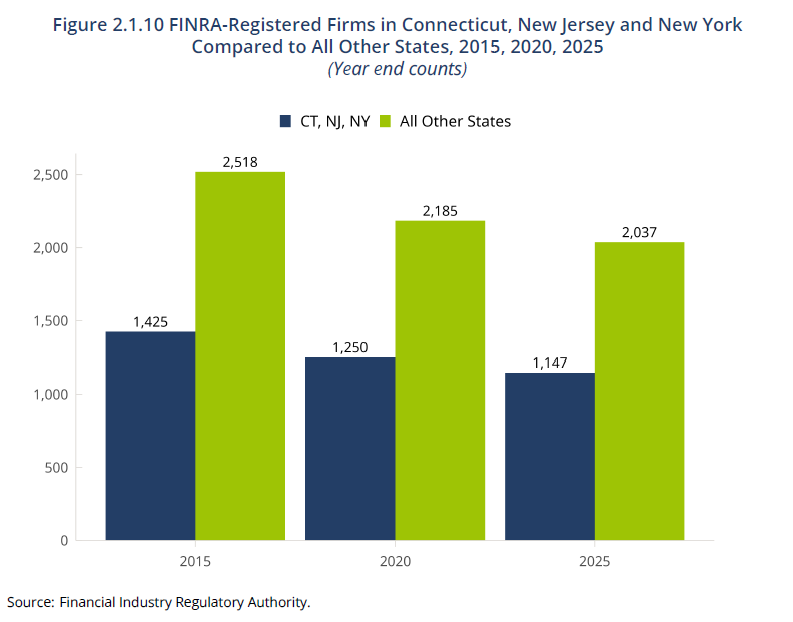

- Figure 2.1.10 FINRA-Registered Firms in Connecticut, New Jersey and New York compared to all other States, 2015, 2020, 2025

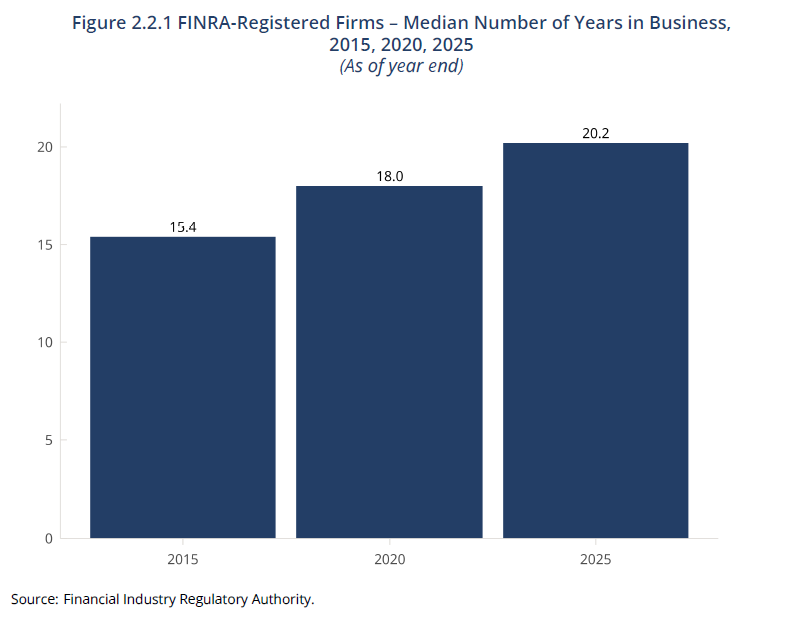

2.2 Entrance and Exit of Firms- Figure 2.2.1 FINRA-Registered Firms – Median Number of Years in Business, 2015, 2020, 2025

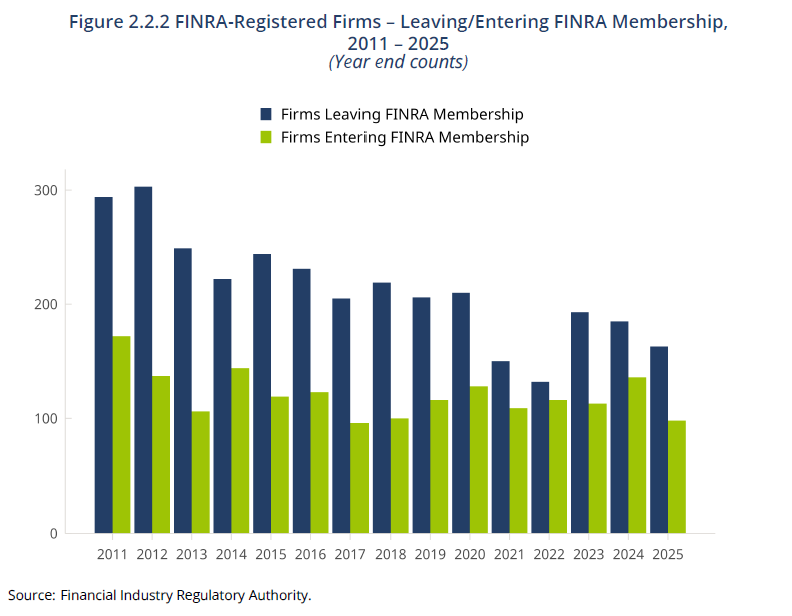

- Figure 2.2.2 FINRA-Registered Firms – Leaving/Entering FINRA Membership, 2011–2025

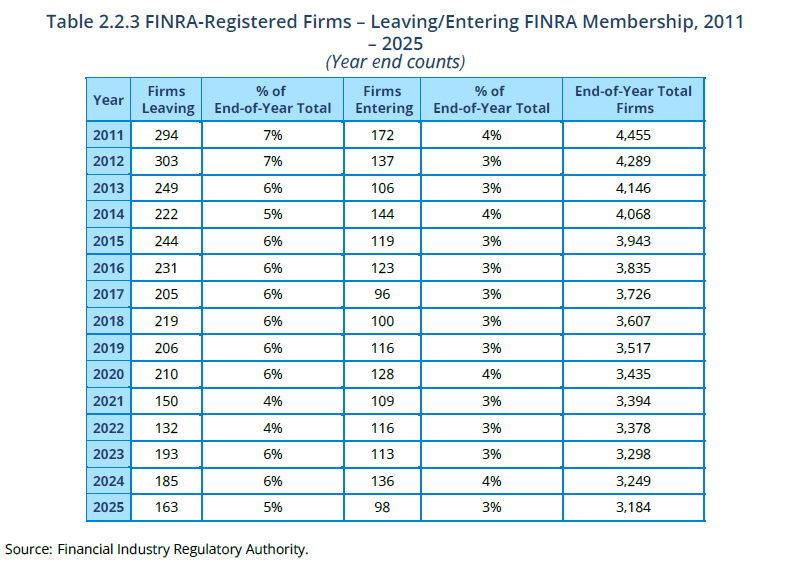

- Table 2.2.3 FINRA-Registered Firms – Leaving/Entering FINRA Membership, 2011–2025

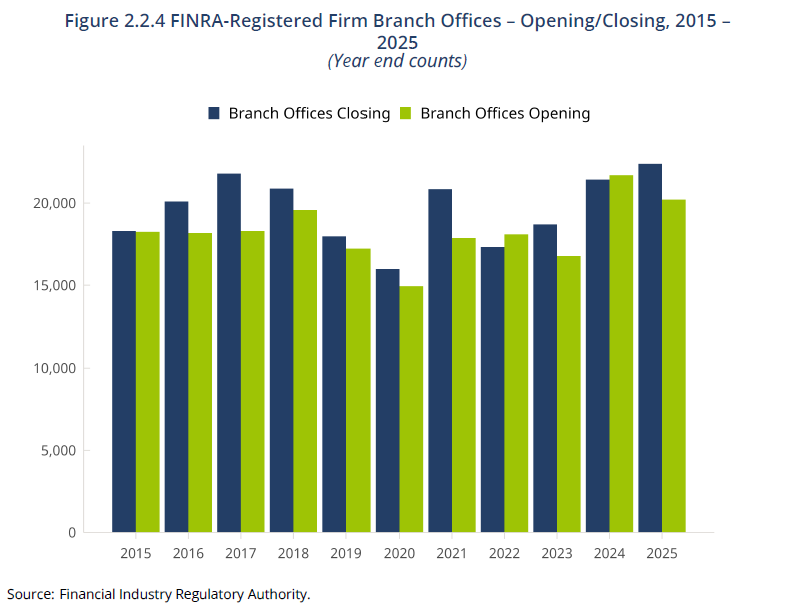

- Figure 2.2.4 FINRA-Registered Firm Branch Offices – Opening/Closing, 2015–2025

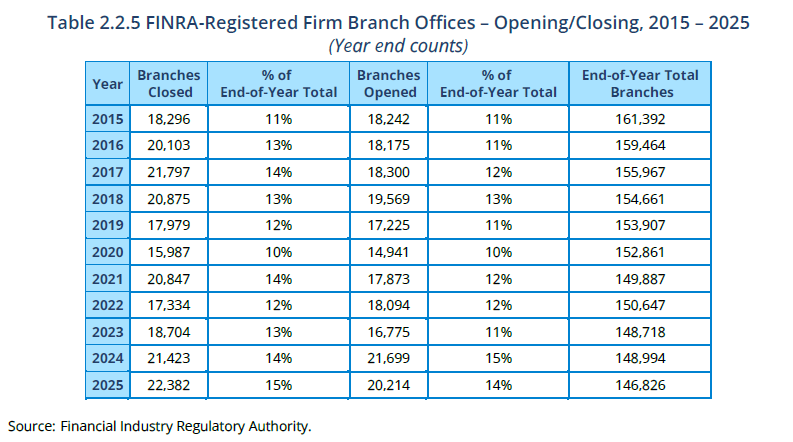

- Table 2.2.5 FINRA-Registered Firm Branch Offices – Opening/Closing, 2015–2025

- Figure 2.3.1 Geographic Distribution of FINRA-Registered Firms by Number of Branches, 2025

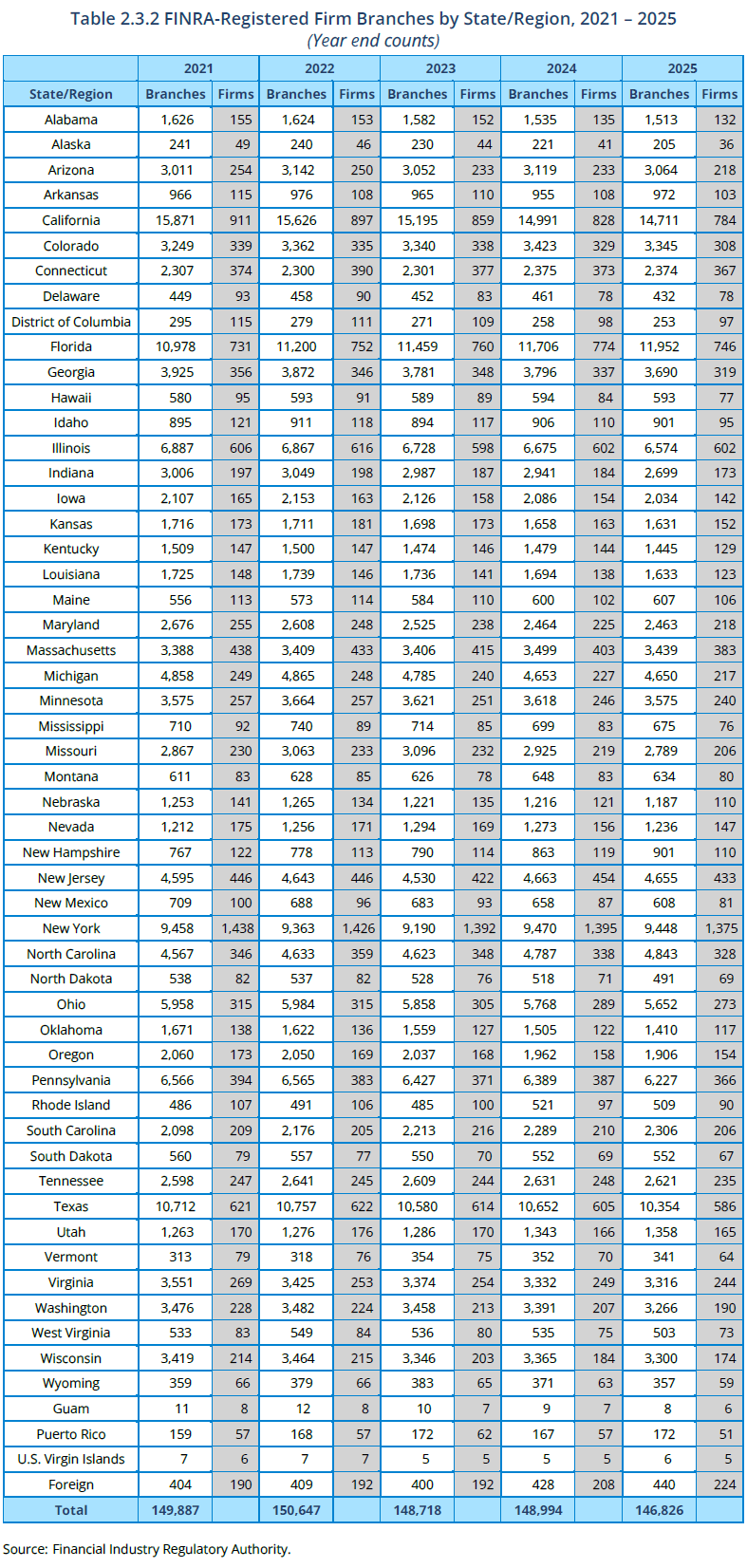

- Table 2.3.2 FINRA-Registered Firm Branches By State/Region, 2021–2025

- Figure 2.3.3 Geographic Distribution of FINRA-Registered Firms by Headquarters, 2025

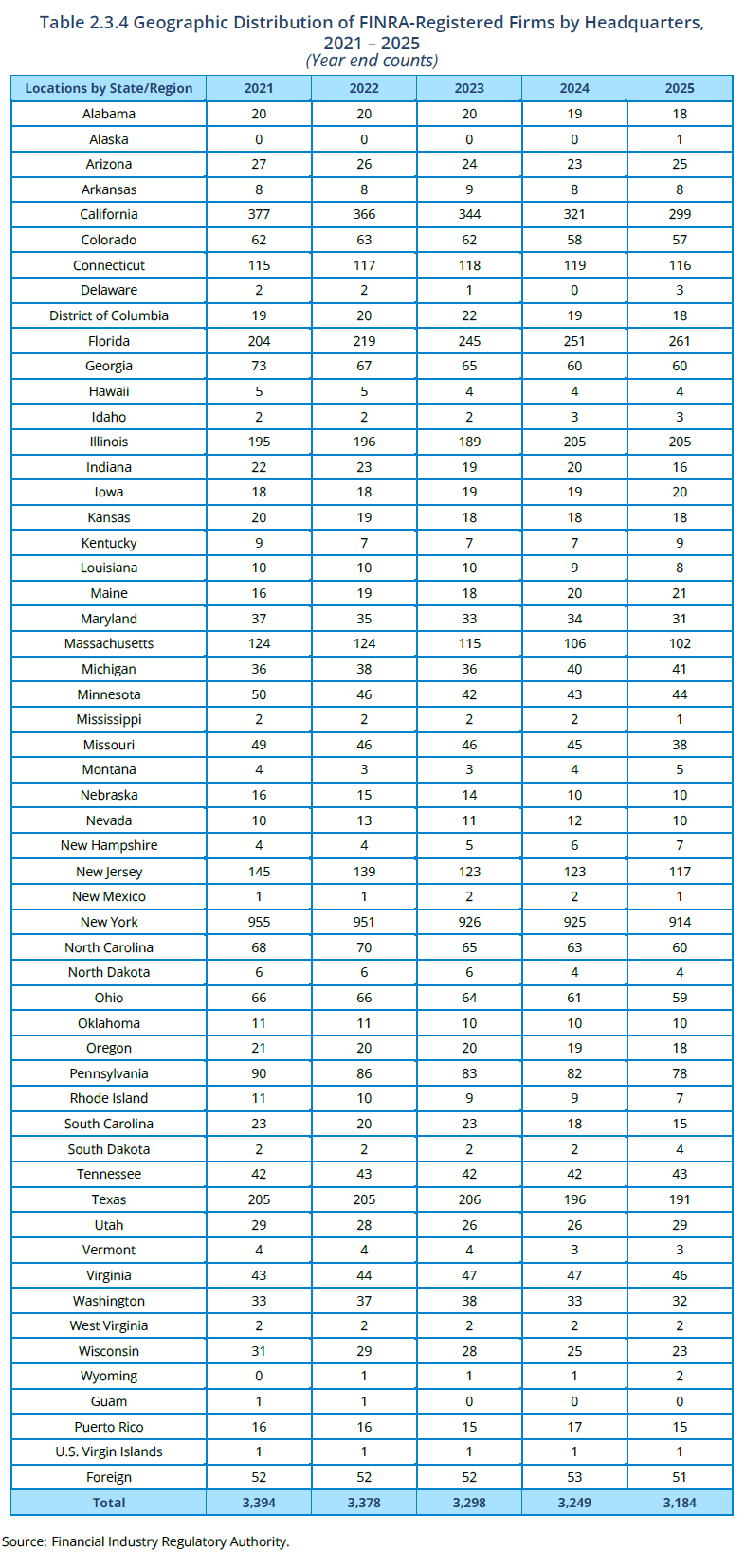

- Table 2.3.4 Geographic Distribution of FINRA-Registered Firms by Headquarters, 2021–2025

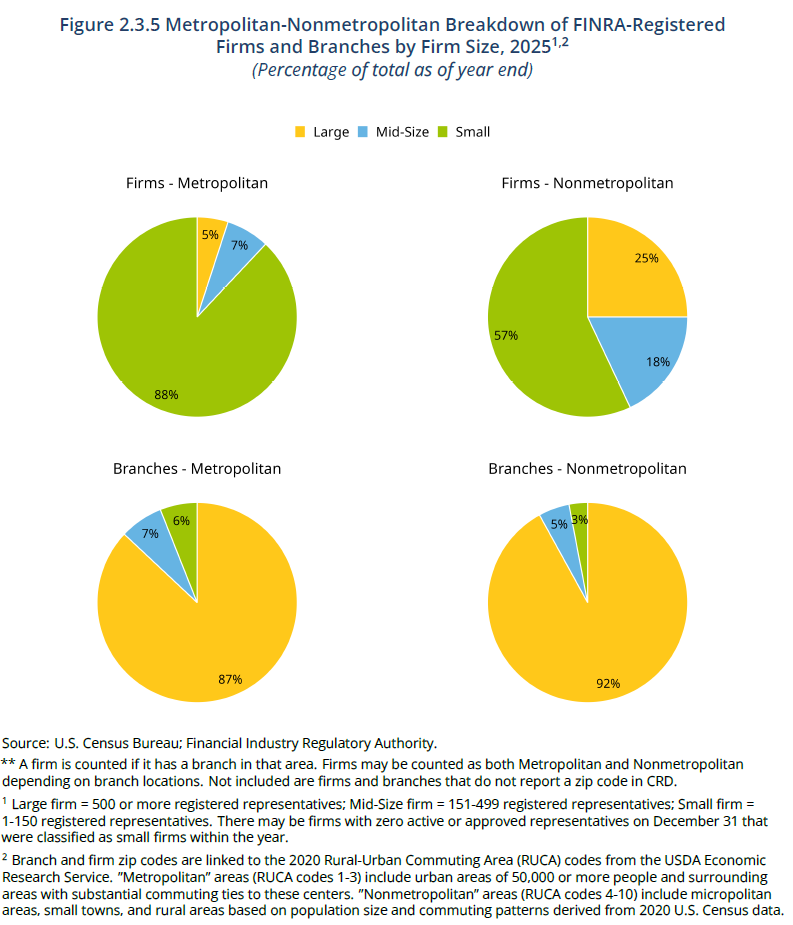

- Figure 2.3.5 Urban-Rural Breakdown of FINRA-Registered Firms and Branches by Firm Size, 2025

- Table 2.3.6 Urban-Rural Breakdown of FINRA-Registered Firms and Branches by Firm Size, 2025

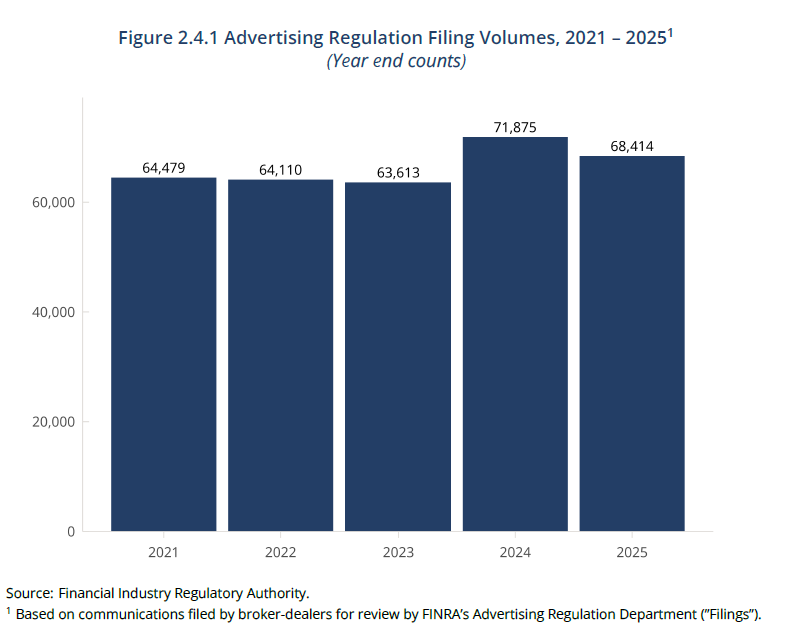

- Figure 2.4.1 Advertising Regulation Filing Volumes, 2021−2025

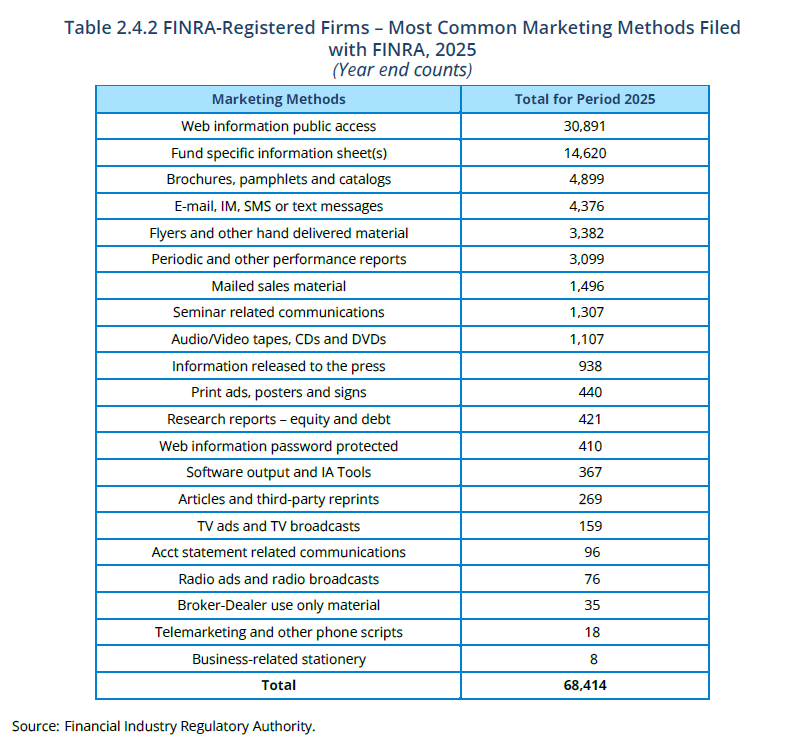

- Table 2.4.2 FINRA-Registered Firms – Most Common Marketing Methods Filed with FINRA, 2025

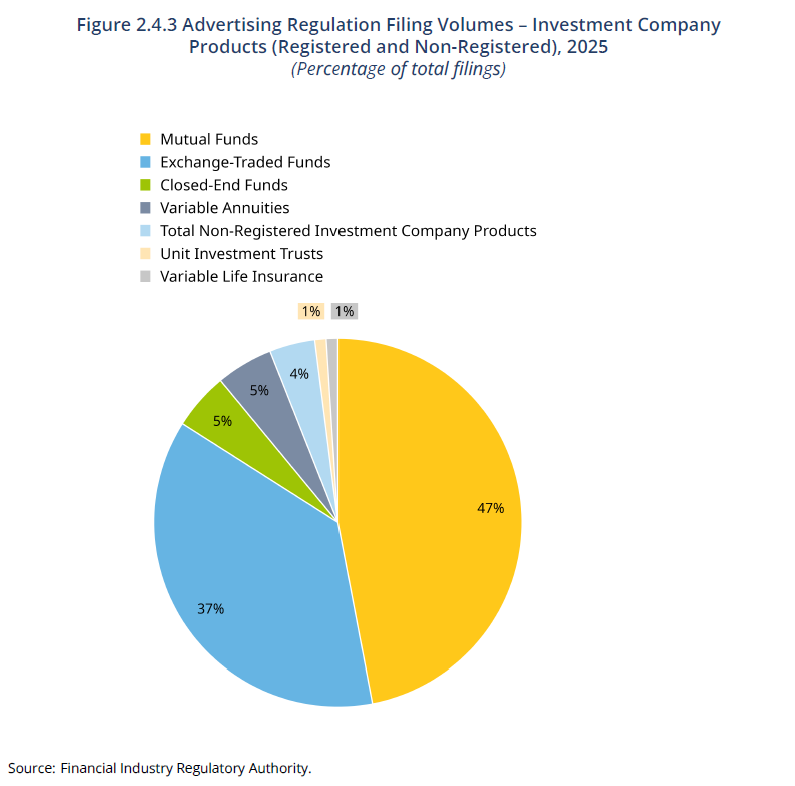

- Figure 2.4.3 Advertising Regulation Filing Volumes – Investment Company Products (Registered and Non-Registered), 2025

- Table 2.4.4 Advertising Regulation Filing Volumes – Investment Company Products (Registered and Non-Registered), 2025

- Table 2.4.5 Advertising Regulation Filing Volumes – Voluntary vs. Mandatory, 2021−2025

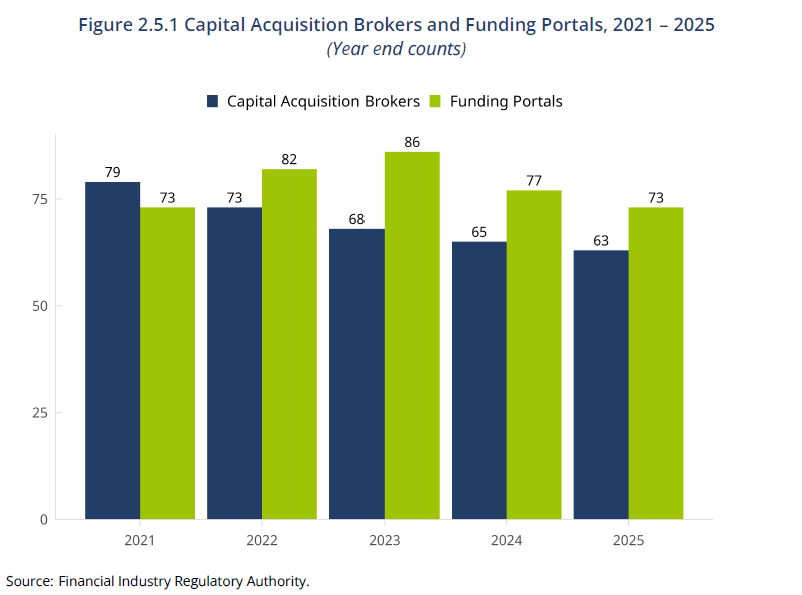

- Figure 2.5.1 Capital Acquisition Brokers and Funding Portals, 2021−2025

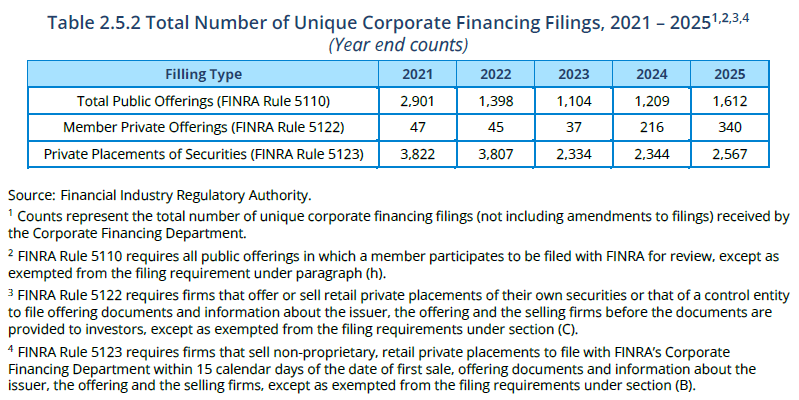

- Table 2.5.2 Total Number of Unique Corporate Financing Filings, 2021−2025

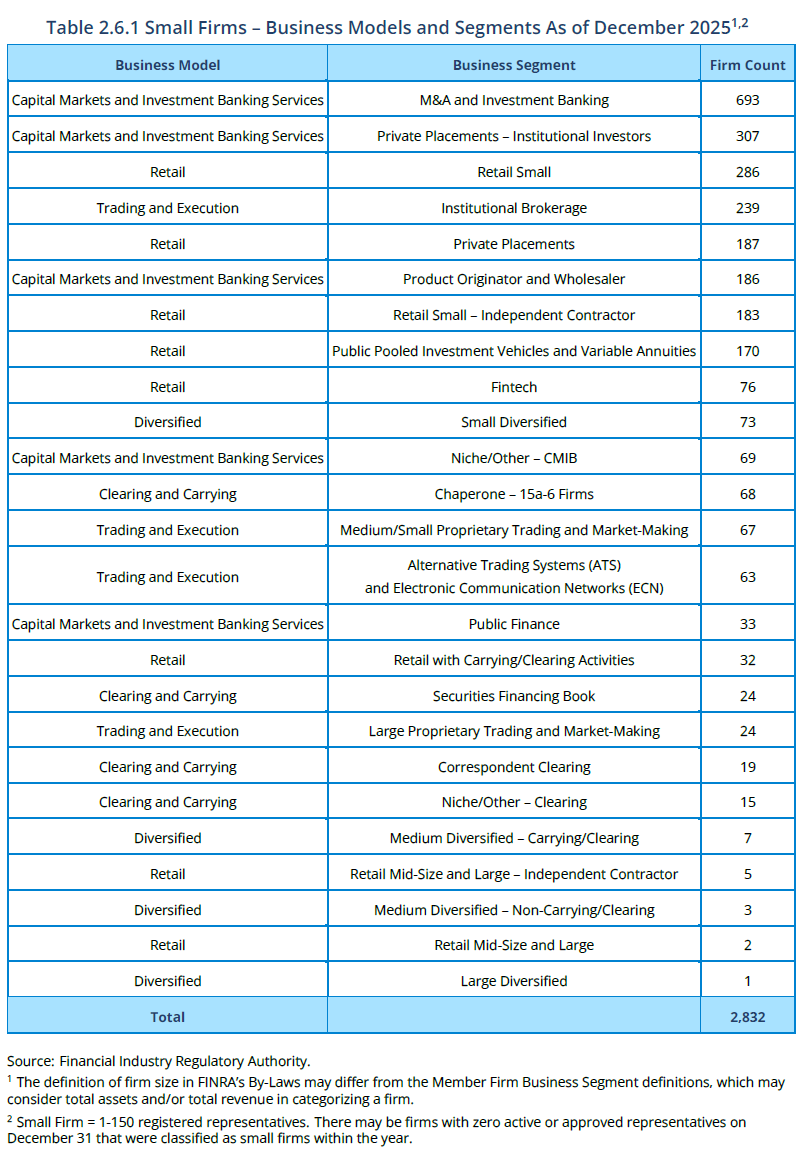

2.6 Business Models and Segments- Table 2.6.1 Small Firms – Business Models and Segments As of December 2025

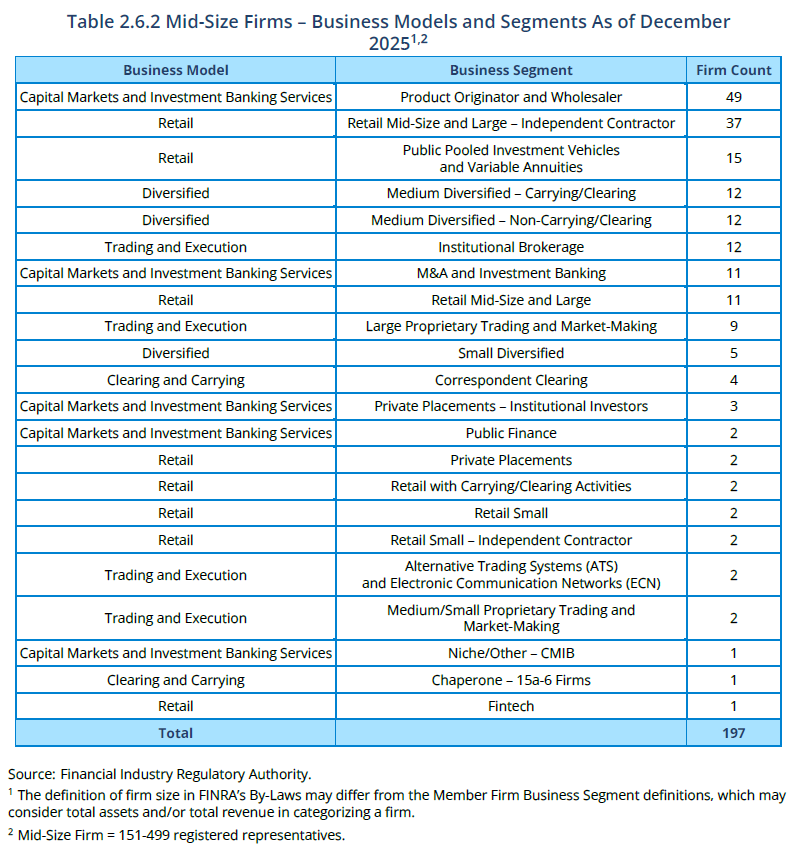

- Table 2.6.2 Mid-Size Firms – Business Models and Segments As of December 2025

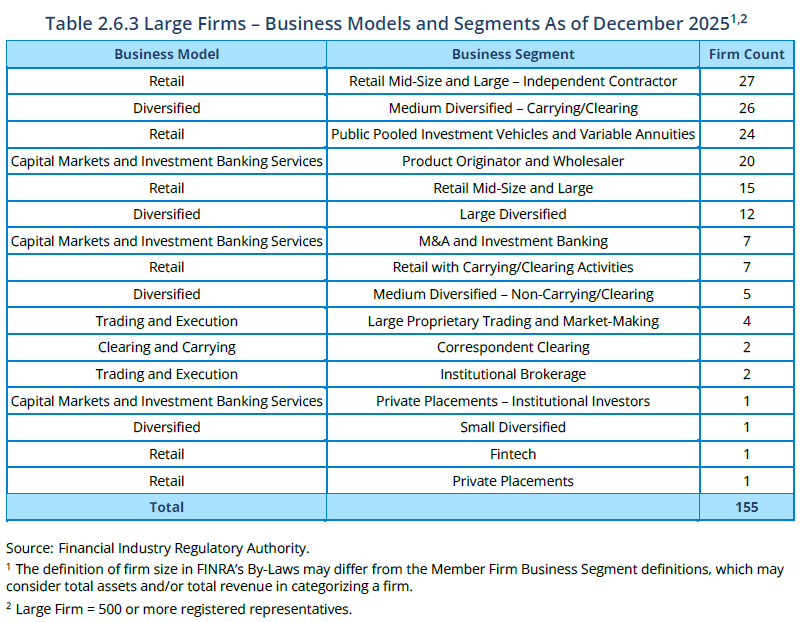

- Table 2.6.3 Large Firms – Business Models and Segments As of December 2025

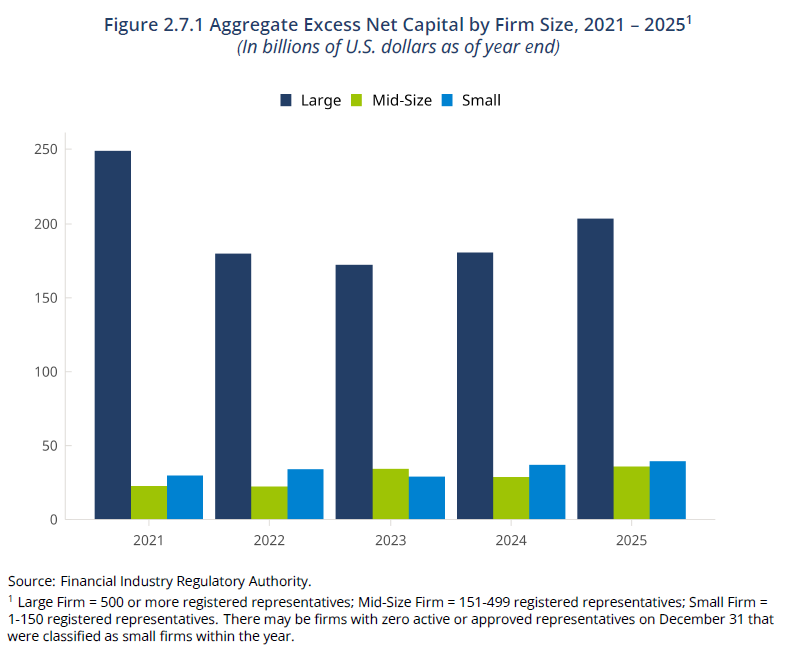

- Figure 2.7.1 Aggregate Excess Net Capital By Firm Size, 2021−2025

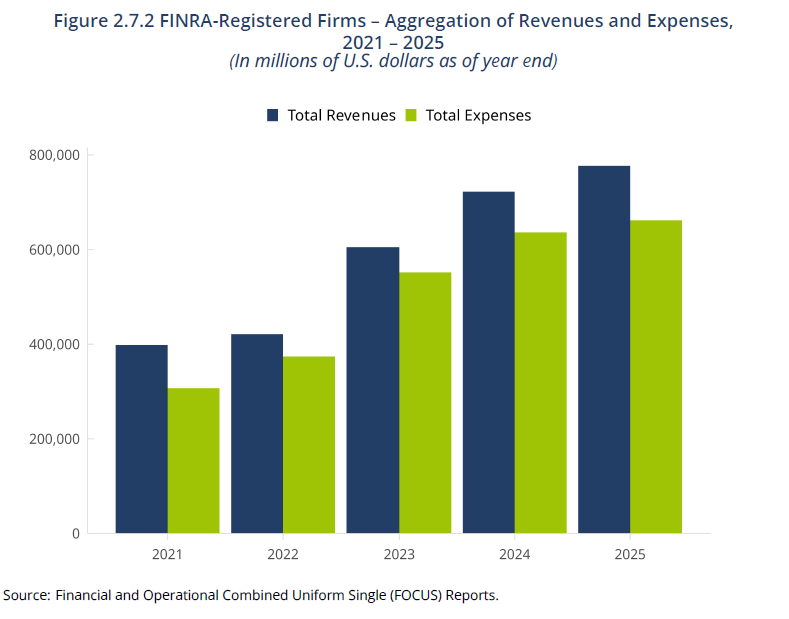

- Figure 2.7.2 FINRA-Registered Firms – Aggregation of Revenues and Expenses, 2021−2025

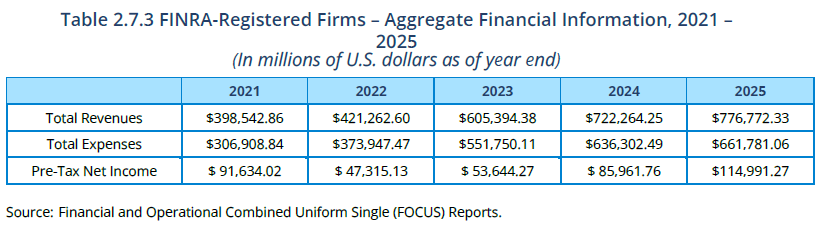

- Table 2.7.3 FINRA-Registered Firms – Aggregate Financial Information, 2021−2025

Firms must be registered with FINRA to conduct securities business with the investing public. Firms must meet certain criteria to attain membership with FINRA, and register with the U.S. Securities an Exchange Commission, other self-regulatory organizations and state regulators. A FINRA member firm’s securities’ activities may include underwriting, trading, sales of securities, and custody of customer assets.

2.1 Sizes and Counts

2.2 Entrance and Exit of Firms

2.3 Geographic Distribution

Figure 2.3.1 Geographic Distribution of FINRA-Registered Firms by Number of Branches, 2024

(See linked page)

Figure 2.3.3 Geographic Distribution of FINRA-Registered Firms by Headquarters, 2024

(See linked page)

2.4 Advertising and Products

FINRA Rule 2210 governs member broker-dealers’ communications with the public, including communications with retail and institutional investors. The rule provides standards for the content, approval, recordkeeping and filing of communications with FINRA. FINRA’s Advertising Regulation Department reviews firms’ advertisements and other communications with the public to ensure they are fair, balanced and not misleading. FINRA rules do not require all communications to be filed, and the figures presented below therefore represent only a segment of such communications.

2.5 Capital Formation

Capital Acquisition Brokers (CABs) engage in a limited range of activities, including advising companies and private equity funds on capital raising and corporate restructuring, and acting as a placement agent for sales of unregistered securities to institutional investors under limited conditions. The CAB rules took effect in 2017. Funding Portals (FPs) also engage in a limited range of activities: those prescribed under the JOBS Act and the SEC’s Regulation Crowdfunding. The FP rules took effect in 2016.

2.6 Business Models and Segments

On October 1, 2018, FINRA announced that it was moving toward an exam and risk monitoring program structure that is based on the business models of the firms FINRA oversees. FINRA has grouped firms according to the primary business(es) in which they are engaged. In 2026, FINRA has further updated its terminology: ’Business Model’ replaces ’Firm Grouping’ and ’Business Segment’ replaces ’Firm Sub-Grouping’; this change is reflected in the 2026 Industry Snapshot. The following tables break down business segments by firm size.

2.7 Financials