How Parties Select Arbitrators

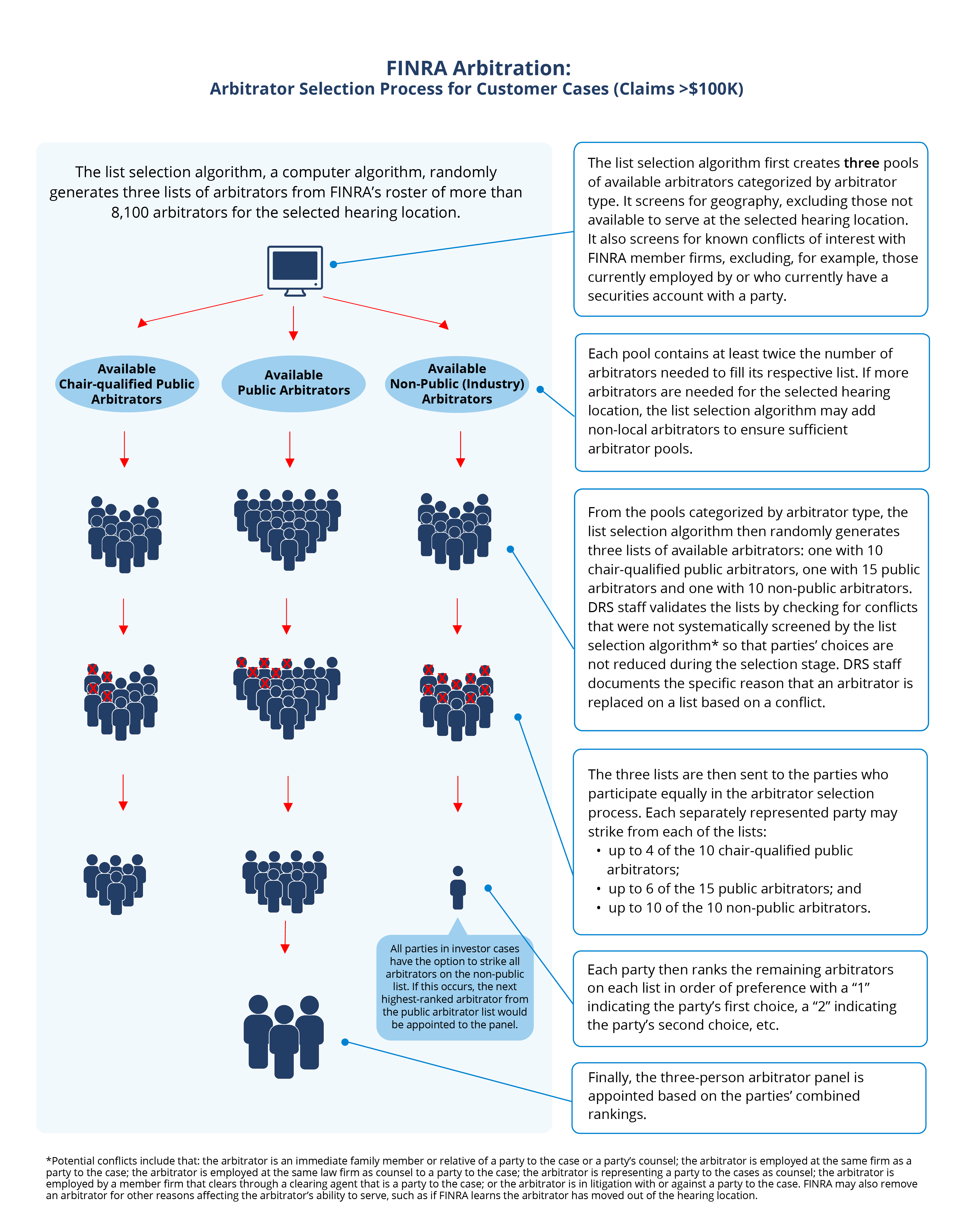

FINRA’s arbitrator appointment process uses the list selection algorithm, a computer algorithm, to randomly generate lists of arbitrators from FINRA’s arbitrator roster. The specific case type will affect the number of lists generated and the number of arbitrator names per list.

FINRA arbitrators are independent and are chosen by the parties to issue final, binding awards. FINRA administers an arbitration forum pursuant to rules approved by the SEC. In its capacity as a neutral administrator of its forum, FINRA does not have any input into the outcome of arbitrations.

Cases Decided by One Arbitrator

For claims of up to $100,000, the case is decided by one arbitrator.

Disputes Involving an Investor, Disputes Between Associated Persons and Disputes Between or Among Brokerage Firms and Associated Persons (That Do Not Contain a Statutory Employment Discrimination Claim)

Definitions

See FINRA Rules 12100(t) and 13100(r) for the definition of non-public arbitrator.

See FINRA Rules 12100(aa) and 13100(x) for the definition of public arbitrator.

See FINRA Rules 12400(c) and 13400(c) for information on how an arbitrator becomes chair-qualified.

The parties will receive one list of 10 chair-qualified public arbitrators. Each separately represented party may strike up to four arbitrators on the list, leaving at least six arbitrator names remaining on each party’s list.

After exercising their strikes, each separately represented party shall rank all remaining arbitrators in order of preference, with a "1" indicating the party's first choice, a "2" indicating the party's second choice, and so on.

The Director of FINRA Dispute Resolution Services (“Director”) will combine the parties’ ranked lists to appoint the chair-qualified public arbitrator based on the parties’ rankings. The Director makes every effort to appoint the highest ranked arbitrators based on the parties’ combined lists. If there is no chair-qualified public arbitrator available to serve from the parties’ combined lists, the Director will appoint a chair-qualified public arbitrator from names generated randomly by the list selection algorithm.

Disputes Between Brokerage Firms (That Do Not Contain a Statutory Employment Discrimination Claim)

This process is the same as above, except the arbitrators will be classified as chair-qualified and non-public.

Investor Cases Decided by Three Arbitrators

For claims more than $100,000, the case is decided by three arbitrators.

The parties will receive three lists of arbitrators:

- One with 10 chair-qualified public arbitrators;

- One with 15 public arbitrators; and

- One with 10 non-public arbitrators.

Each separately represented party may strike:

- Up to four of the 10 arbitrators on the chair-qualified public list for any reason (at least six names must remain on this list);

- Up to six of the 15 arbitrators on the public list for any reason (at least nine names must remain on this list); and

- Up to all 10 arbitrators on the non-public list.

After exercising their strikes, each separately represented party shall rank all remaining arbitrators on the lists in order of preference with a "1" indicating the party's first choice, a "2" indicating the party's second choice, and so on. Each list of arbitrators must be ranked separately.

The Director will combine the parties’ ranked lists to appoint the panelists based on the parties’ rankings. The Director makes every effort to appoint the highest ranked arbitrators based on the parties’ combined lists. If there are not sufficient arbitrators available to serve from the combined chair-qualified public list or public list, the Director will appoint an arbitrator(s) of the required classification from names generated randomly by the list selection algorithm.

Arbitrator Appointment When All Non-Public Arbitrators Have Been Stricken

If the parties collectively strike all the non-public arbitrators, or if all ranked non-public arbitrators are not available to serve, the Director will select the next highest-ranked public arbitrator to complete the panel.

If the public list is exhausted, the Director will select the next highest-ranked arbitrator on the chair-qualified public list. If the chair-qualified public list is exhausted, the Director will appoint a public arbitrator from names generated randomly by the list selection algorithm.

Conflicts of Interest

The list selection algorithm automatically excludes arbitrators from the lists based upon known conflicts of interest with member firms, such as when the arbitrator is currently employed by or currently has a securities account with a member firm that is a party to the case. FINRA staff then conducts a final review to check for other known current conflicts that cannot be systematically screened by the list selection algorithm so that the parties’ choices are not reduced during the selection stage. These types of conflicts include an arbitrator employed by a party to the case; an arbitrator who is an immediate family member or relative of a party to the case or a party’s counsel; an arbitrator employed at the same firm as a party to the case; an arbitrator employed at the same law firm as counsel to a party to the case; an arbitrator representing a party to the case as counsel; an arbitrator who is an account holder with a party to the case; an arbitrator employed by a member firm that clears through a clearing agent that is a party to the case; or an arbitrator in litigation with or against a party to the case. FINRA may also remove an arbitrator for other reasons affecting the arbitrator's ability to serve, such as if FINRA learns the arbitrator has moved out of the hearing location. FINRA staff document in writing the specific reason that an arbitrator is replaced on a list based on a current conflict.

Selection Pools to Populate Arbitrator Lists

FINRA makes arbitrator applicants available to appear on case lists after applicants have:

- completed the required application and background check;

- been approved by the Neutral Roster Subcommittee of the National Arbitration and Mediation Committee (NAMC); and

- completed FINRA’s Basic Arbitrator Training Program, which includes the online basic arbitrator and expungement trainings.

FINRA will assign an arbitrator to one primary hearing location, which is the hearing location closest to the arbitrator’s primary residence.

To populate the lists, the list selection algorithm requires a minimum number of available arbitrators (“pool”) from which to randomly select names. This pool size is equal to the number of arbitrators needed to fill a standard list, multiplied by two. For example, in a customer case decided by three arbitrators (which will have 10 names on the chair-qualified public arbitrator list; 15 names on the public arbitrator list; and 10 names on the non-public arbitrator list), the list selection algorithm requires a pool size for each list of: 20 chair-qualified public arbitrators; 30 public arbitrators; and 20 non-public arbitrators. A chair-qualified public arbitrator is eligible to appear on both the chair-qualified public arbitrator list and the public arbitrator list (but not in the same case).

The List Selection Algorithm Random List Selection Process

The list selection algorithm arbitrator list selection process is random. KPMG performed a procedural and technical review of the list selection algorithm and issued a report in October 2023.

The list selection algorithm uses up to three “passes” to ensure that there is a sufficient arbitrator pool from which to generate random lists:

Pass One – All Local Arbitrators

A list will be populated on the first pass when the list selection algorithm can select from a local pool of at least two times the number of required arbitrators per list. A local arbitrator is one who serves in the hearing location closest to their primary address. If there are multiple hearing locations within 75 miles of an arbitrator’s primary address, the arbitrator is considered local to each of those hearing locations.

Pass Two – Arbitrators Traveling at FINRA’s Expense

If local arbitrators alone cannot fill the minimum pool, the list selection algorithm will supplement the pool by adding arbitrators from other hearing locations who previously agreed to travel at FINRA’s expense to that hearing location.

Pass Three – Arbitrators Not Pre-Screened to Travel

In extremely rare circumstances, the first two passes will not be sufficient to fill the pool. If so, FINRA staff will designate additional hearing locations from which the list selection algorithm can randomly select arbitrators. However, the arbitrators in these locations are not pre-screened with respect to their willingness to travel to the hearing.

Continual Monitoring to Ensure Sufficient Pool Sizes

FINRA staff routinely analyzes the number of available arbitrators of each classification (i.e., public or non-public) in each of FINRA’s hearing locations. This analysis ensures that there will be enough available arbitrators for panel selection in each hearing location. If FINRA staff determine that additional public or non-public arbitrators are needed in a specific hearing location, all arbitrators of the required classification in an alternate hearing location are invited to travel at FINRA’s expense. All arbitrators who agree to travel at FINRA’s expense are designated accordingly by the list selection algorithm and only supplement local pools when a local pool is insufficient to populate the required list.

For reference, a complete breakdown of the number and classification of available arbitrators in each hearing location is available on FINRA’s Dispute Resolution Statistics Web page, which is updated monthly. The hearing location chart reflects the number of local and non-local arbitrators available in each hearing location.

Other Types of Intra-Industry Claims

For arbitration claims that involve only industry parties and that involve a statutory employment discrimination claim, promissory note proceedings, or permanent injunctive relief, please refer to the appropriate rule for the arbitrator selection rules:

- Statutory Employment Discrimination (Rule 13802);

- Promissory Note Proceedings (Rule 13807); or

- Permanent Injunctive Relief (Rule 13804).

Party Requests for Additional Arbitrator Information

If a party requests additional information about an arbitrator, FINRA will anonymously request the additional information from the arbitrator unless an opposing party objects to the request within ten days of its receipt. The requesting party may withdraw the request within five days of receipt of the objection.

FINRA will not extend the time for parties to return the ranking form when a party requests additional information from an arbitrator. However, parties may agree to extend the deadline for ranking forms or shorten the time allowed for an objection or withdrawal after an objection.

Challenges to Arbitrators

In addition to allowing parties to strike proposed arbitrators on the ranking lists prior to appointment, FINRA rules also provide parties with the right to challenge arbitrators for cause. If a party believes that FINRA has incorrectly listed an arbitrator on a ranking list, it may: (1) file a motion with the Director of Dispute Resolution (Director) under Rule 12503(e)(1)/13503(e)(1) requesting that the Director remove the arbitrator from the ranking list, or (2) request that the opposing party agree to remove the arbitrator from the ranking list.

The term "hearing session" means any meeting between the parties and arbitrator(s) of four hours or less, including a hearing or a prehearing conference.

After the Director sends the ranking lists to the parties, but before the first hearing session begins, FINRA rules provide that the Director will grant a party’s request to remove an arbitrator if it is reasonable to infer, based on information known at the time of the request, that the arbitrator is biased, lacks impartiality, or has a direct or indirect interest in the outcome of the arbitration. The interest or bias must be definite and capable of reasonable demonstration, rather than remote or speculative. FINRA rules also provide that close questions regarding challenges to an arbitrator made by a customer will be resolved in favor of the customer.

After the first hearing session begins, the Director may remove an arbitrator based only on information required to be disclosed under Rule 12405 that was not previously known by the parties. The Director may exercise this authority upon request of a party or on the Director's own initiative.

The following list, though not exhaustive, provides examples of causal challenges under FINRA Rule 12407(a).

Please consult FINRA Rules 12503 and 13503 for motion deadlines.

Opinion and Bias

- Arbitrator has a firm opinion or belief as to the subject of a case for which he or she is an arbitrator.

- Arbitrator has a personal bias toward a party or party representative.

Personal Relationships

- Arbitrator is or was related by blood or marriage to a party, its attorneys or witnesses.

- Arbitrator is or was a party's guardian.

Business Relationships

- Arbitrator is or was a business partner or vendor of a party.

- Arbitrator is a customer or client of a party.

- Arbitrator was a customer or client of a party in the past five (5) years.

- Arbitrator was a customer or client of a party for more than fifteen (15) years.

- Arbitrator is a surety or guarantor of the obligations of a party.

- Arbitrator is currently a creditor or shareholder of any corporate party, or has any business relationship with a party.

- Arbitrator is or was a conservator or conservatee, employer or employee, principal or agent, or debtor or creditor of either a party or an officer of a corporation which is a party.

- Arbitrator is the parent, spouse or child of a person who is or was a conservator or conservatee, employer or employee, principal or agent, or debtor or creditor of either a party or an officer of a corporation which is a party.

Current Involvement

- Arbitrator is adverse to a party, its attorneys or witnesses.

- Arbitrator is a party to or the subject of a complaint, arbitration or litigation involving a securities investment.

- Arbitrator is currently an expert witness for a party.

Previous Involvement

- A motion to vacate challenging an award in a case in which the arbitrator had participated and signed the award that was filed by a party, its attorneys, or witnesses was granted.

- Arbitrator issued a complaint against a party, its attorneys or witnesses, in an action instituted or resolved during the past five (5) years.

- Arbitrator or any member, shareholder or associate of, or of counsel to his or her law firm, has had an attorney/client relationship with a party within three (3) years of the filing of the arbitration claim.

- Arbitrator or any member, shareholder or associate of, or of counsel to his or her law firm, has had an attorney/client relationship adverse to a party within three (3) years of the filing of the arbitration claim.

Financial Interest

- Arbitrator knows that he or she has, individually or as a fiduciary, a financial interest in the subject matter in controversy or in a party in the arbitration proceeding, or any other interest that could be substantially affected by the outcome of the arbitration proceeding.

- Arbitrator's immediate family member (as defined in Rule 12100) has a financial interest in the subject matter in controversy or in a party in the arbitration proceeding, or any other interest that could be substantially affected by the outcome of the arbitration proceeding.

Expert Witnesses

- An arbitrator in this matter testified as an expert witness against a party during the past (5) years.

- An arbitrator in this matter testified as an expert witness for a party during the past (5) years.

- An arbitrator in this matter was retained as an expert witness (but did not testify) in an action involving a party during the past three (3) years.

- An arbitrator in this matter was retained as an expert witness by a party's counsel, or his or her law firm, in an action during the past three (3) years (where no party in this matter was involved in the earlier action).

Parties may not inform the panel of an opposing party’s casual challenge. If a party does so, the opposing party may challenge the arbitrator within five days of being made aware of the disclosure. Absent extraordinary circumstances, the Director will grant the challenge when timely filed. If the challenge is not timely filed, the opportunity is forfeited.